Insights and Observations

Economic, Public Policy, and Fed Developments

- The biggest rate surprise last month came not from the US, but the UK. Prime Minister Liz Truss’s unexpectedly large, proposed tax cuts had the government engaged in stimulus while the Bank of England (BOE) was tightening, and adverse market reaction led to a collapse in the pound and a surge in Gilts. This briefly pushed the UST 10Yr above 4% intraday for the first time since 2010 until the BOE, fearing a collapse in leveraged pension funds, stepped in with another round of quantitative easing. This stabilized UK rates but will do little to quell inflation.

- This all came after an eventful start to the month. After welcome improvement in July, too-hot August CPI and PPI reports upwardly recalibrated market expectations for Fed Funds policy. Below the surface it was not all bleak – the percentage of CPI components increasing at an annualized rate greater than 4.0% fell to 71%. And, while the shelter component had the highest monthly print since 1991 at +0.69%, this represents a six-month rolling average and July and August median house price declines were the largest since 2009, suggesting a downward near-term trend.

- The Producer Price Index (PPI) garnered attention as core inflation surprised higher by a tenth to +0.4% month-over-month. Services inflation (+0.4%) was largely responsible, and with 60% of that gain attributable to a category including labor costs there was talk of a potential wage price spiral. However, two-thirds of the increase came from fuel and lubricants, and we believe the more likely explanation for PPI is that gas prices track oil price increases rapidly but decreases are reflected more slowly. This too should ease in coming months. Still, like CPI, this was hardly an inflation report the Fed was hoping to see.

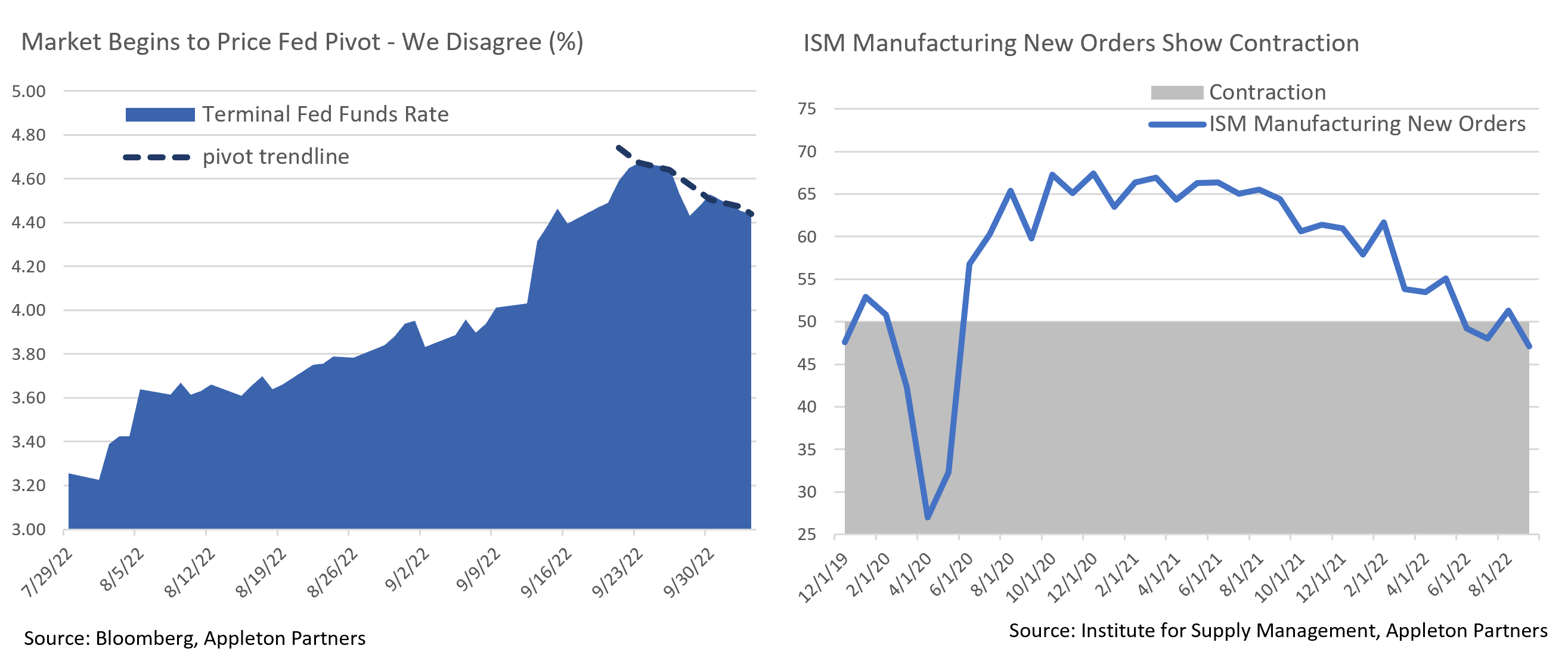

- The annual GDP re-benchmarking further complicates the Fed’s job. While 2022 headline growth was unchanged, revisions show an increase in consumer spending from 3Q ‘21 through 2Q ‘22, coupled with upwards inventory revisions to the most recent periods. Consumer spending now exceeds aggregate supply by an even greater margin, and it will likely require proportionately more action from the Fed to rebalance to supply. Inventories are sensitive to short-term funding rates, and companies will have incentive to right-size inventory. This would detract from GDP and make a recession harder to avoid. Evidence of this is already evident in the ISM Manufacturing Index, which fell to just above contraction territory in September.

- Labor conditions are still strong, and Friday’s employment report forecast calls for an additional 265k new jobs. Hiring is occurring amid economic weakness because employers were badly short-staffed going into the slowdown and even depressed conditions have not changed that situation. The JOLTS survey showed the ratio of openings to unemployed fell sharply from 1.97 to 1.67 in August, although these are elevated levels. We expect hiring to remain resilient for several more months, but when it does slow it is likely to be abrupt.

- Despite a bleak macro environment, in the relative calm following the BOE intervention markets have begun to price a future Fed pivot and a moderation of terminal Fed Funds rates, with equities rebounding strongly as October trading began. We believe these monetary policy expectations are misguided; the Fed has been clear they will hike until inflation has fallen materially from current levels.

From the Trading Desk

Municipal Markets

- Municipal bond price declines accelerated in September with the Bloomberg Barclays Managed Money Short/Intermediate Index falling by 3.05%. Tax-exempt yields ended Q3 at highs not seen in many years with 2-year AAAs at 3.09%, the highest rate since December of 2007, while 10-year AAA bonds yielded 3.30%, the highest level since early 2009. Income streams have increased dramatically with 2 and 10-year AAA yields equating to 5.47% and 5.78% respectively on a tax-equivalent basis.1

- The municipal curve remains steep relative to USTs but is relatively flat by historical standards. The 10-year Muni/UST ratio at quarter-end was 86.2%, slightly above long-term norms. During rate hike periods over the past few decades, ratios generally declined leaving tax-exempt valuations somewhat rich versus similar duration high quality taxable bonds, a dynamic we have not seen this cycle.

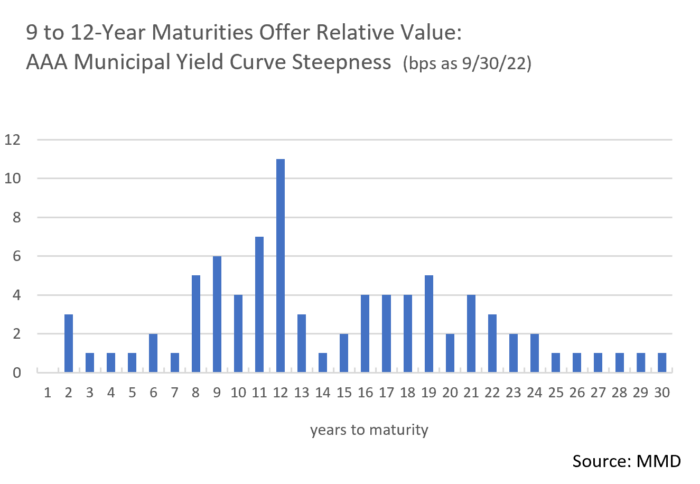

- Our typical intermediate maturity target range has been pushed out a bit as we are finding the greatest relative value among 9 to 12–year maturities. Although short maturity yields jumped by 80 bps in September, UST yields rose even more sharply, and we now see greater opportunity farther out on the curve.

- A highly volatile market characterized by rising yields coupled with strong balance sheets has suppressed municipal issuance. New issuance in September fell 43% YoY and 26% QTD. This has reduced primary market bond availability and pushed more of our buying into the secondary market.

- The positive effect of sluggish issuance on technical factors has been more than offset by mutual funds incurring $91.5B of YTD net outflows, reversing 2021’s strong inflows. We expect flows to return as markets settle, particularly given current yield levels.

Corporate Bond Markets

- Investment Grade primary market issuance missed September expectations by nearly 50% as trading volatility and higher rates drove funding costs to levels not seen since 2009. September is typically packed with deals – new issuance averages ~$150 billion – although last month’s $78.6 billion came up far short. Concessions needed to get deals done have remained well above average, adding to the cost of new debt and discouraging issuance. On a more positive note, most deals have done well as they break out into the secondary market, suggesting there is still appetite for credit. Looking ahead, market syndicates have cautiously projected another $75 billion of new debt in October and a below average Q4.

- Investment Grade credit spreads touched YTD highs in a risk-off final week of September, but quickly retraced to end 6 bps below a YTD peak of 164 bps on the Bloomberg Barclays US IG Corporate Index. Supply limitations have helped keep spreads range bound, although lack of market conviction across the rating spectrum is producing periodic volatility swings.

- Lagging retail fund flows reflect recent market jitters. Investors redeemed $10.3 billion (3rd largest redemption on record) from IG funds over the last week of September. YTD net outflows now stand at $100.3 billion, an indication of weak market sentiment. We feel outflows are likely to continue with high levels of market volatility and economic uncertainty expected over the near-term.

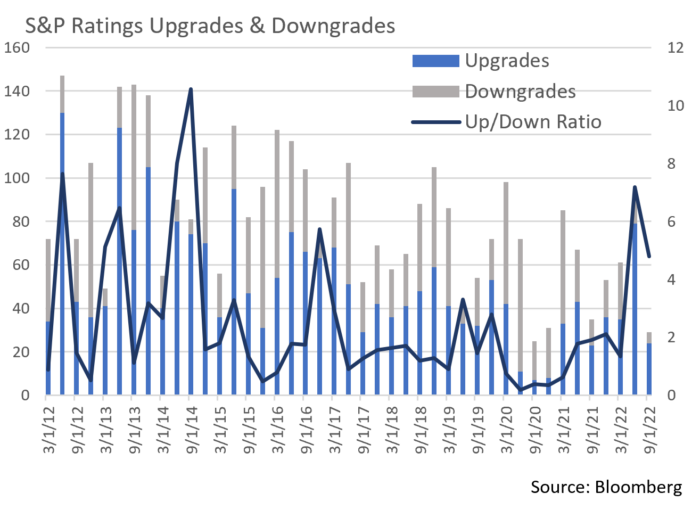

- Corporate credit fundamentals generally remain healthy, and this offers support for credit spreads in the face of a challenging interest rate and technical environment.There have been 138 upgrades and only 42 downgrades YTD, raising the upgrade/downgrade ratio to a vibrant 3.29x, the highest level since 2014. High Yield presents quite a contrast, with 262 upgrades and 265 downgrades, an almost 1:1 ratio.

- Upcoming quarters will prove to be interesting as recession fears, inflation, and growth concerns remain top of mind and may pressure the Investment Grade market. In our view, high quality issuer fundamentals should remain solid and downgrade pressures will most likely come among credits tipping over the IG/HY threshold.

Public Sector Watch

Credit Comments

Hurricane Fiona Exposes the Fragility of Puerto Rico’s Power Grid

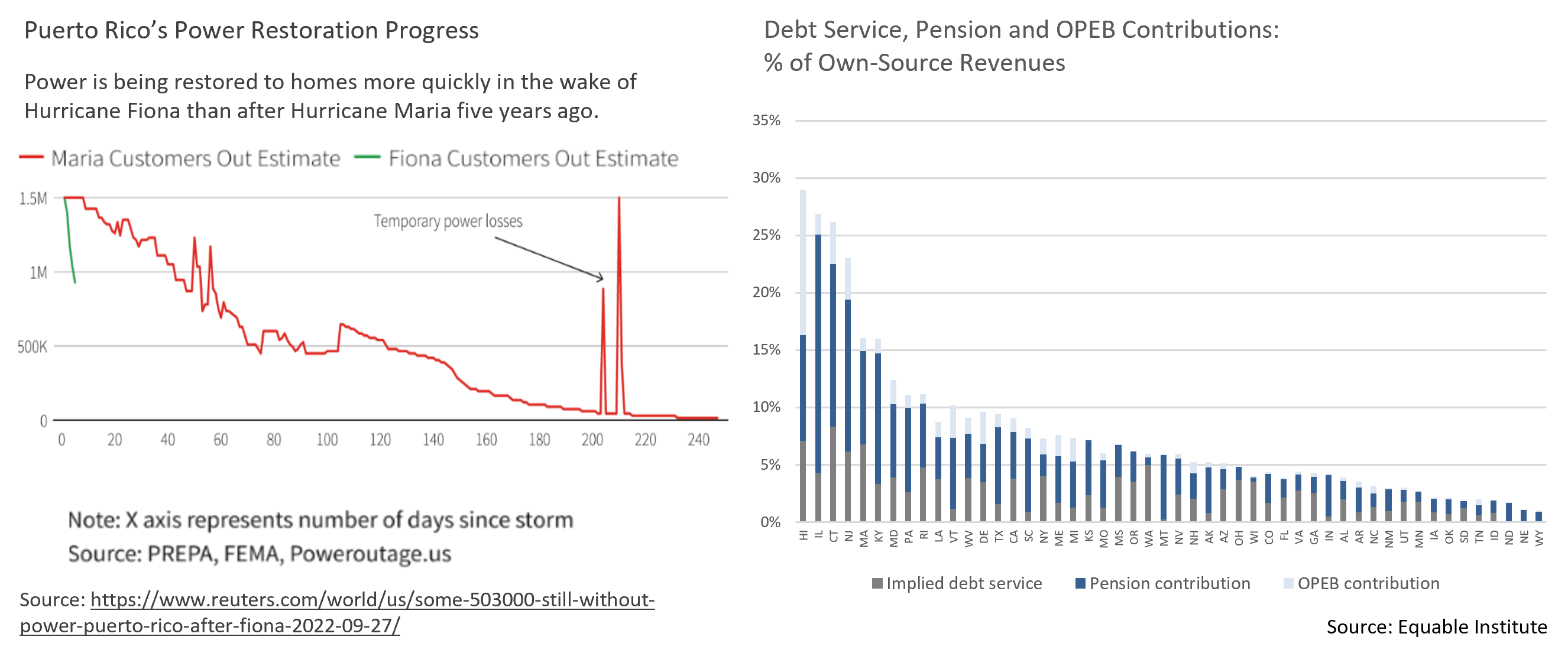

- Perhaps overlooked to an extent given more recent focus on Hurricane Ian, Fiona made landfall in Puerto Rico on September 18th. While wind speeds did not compare to those of Maria five years prior, damage from extreme rain produced landslides and mudslides, flooded neighborhoods, and caused an island-wide blackout.

- More than 746,000 of 1.15 million utility customers in the region were still without power over a week after the hurricane hit, raising questions about billions of dollars of federal aid and whether Puerto Rico’s power grid has materially improved since Hurricane Maria.

- While the Puerto Rico Electric Power Authority, or PREPA, still owns much of the power infrastructure, LUMA, a private company, started managing the system in 2021 as part of PREPA’s debt restructuring. As with PREPA, grid mismanagement remains a concern. Leading up to the storm, increasingly frequent blackouts, voltage fluctuations, and rising energy prices prompted mass protests. Management missteps come at a crucial time with LUMA’s initial contract up for renewal in November, a deal that would lock in the utility for another 15 years.

- US District Court Judge Laura Taylor Swain is working to mediate PREPA’s bankruptcy and recently set a December 1st deadline for a new plan to reduce $9 billion of PREPA debt. The success of PREPA’s restructuring hinges on whether it can reduce its obligations sufficiently to repay its debt while also compensating creditors, some of whom have not been paid in eight years.

- Hurricane Fiona exposed the fragility of Puerto Rico’s power grid, and improvements are still badly needed despite sizeable post- Hurricane Maria federal aid. The outcome of PREPA’s bankruptcy and current operating contracts will be critical to the power grid’s future and its ability to improve reliability.

- Puerto Rico’s power grid serves as an example of the importance of maintenance and sustained infrastructure investment. Extreme weather events such as hurricanes, flooding, wildfires, and heatwaves are increasing in frequency and intensity due to climate change. Power systems must demonstrate the ability and willingness to mitigate blackout and other storm impact given the human cost and economic implications of such events. We see this as an important credit risk factor.

Surging Revenue Outpaces Increased Fiscal 2021 State Liabilities

- Moody’s recently reported that debt, pension and OPEB liabilities all increased in fiscal 2021. Pension obligations easily remain the largest liability of most states, increasing by $1.97 trillion, or +21% YoY. The increase is attributed to lower interest rates in 2020, the measurement period driving most states’ fiscal 2021 reporting. Fiscal 2022 net pension liabilities will decrease due to significant improvement in investment returns, before rising again due to poor 2022 market performance.

- Net tax-supported debt, the second largest liability for most states, also rose in fiscal 2021, although at a slower +3.5% YoY pace.

- Capacity to service fixed costs improved in fiscal 2021 as state revenue surged. The median ratio of total fixed costs to own-source revenue fell to 6.3%, down from 7.4% in the prior fiscal year, evidencing the strong credit position most states enjoy following a windfall of tax revenues.

Strategy Overview

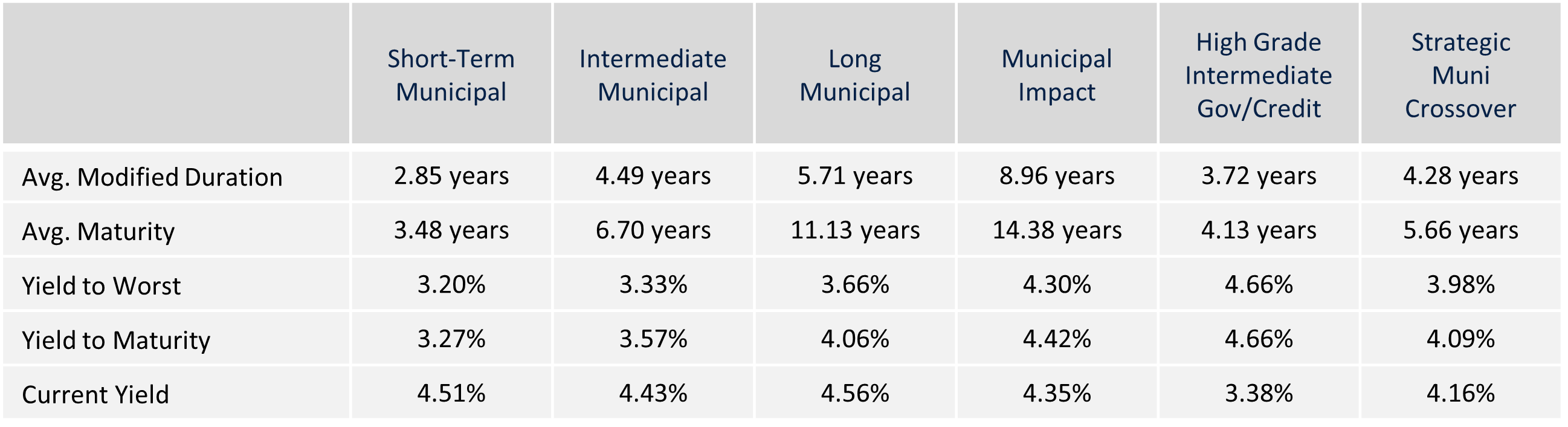

Composite Portfolio Positioning as of 9/30/2022

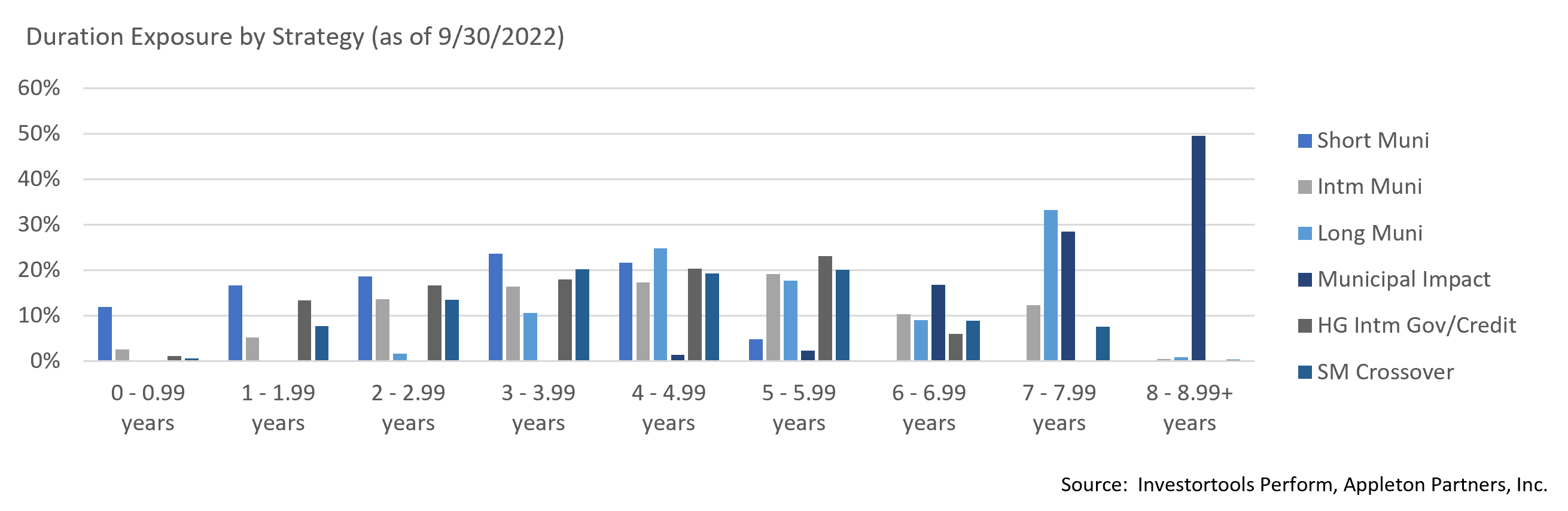

Duration Exposure as of 9/30/2022

Our Philosophy and Process

- Our objective is to preserve and grow your clients’ capital in a tax efficient manner.

- Dynamic active management and an emphasis on liquidity affords us the flexibility to react to changes in the credit, interest rate and yield curve environments.

- Dissecting the yield curve to target maturity exposure can help us capture value and capitalize on market inefficiencies as rate cycles change.

- Customized separate accounts are structured to meet your clients’ evolving tax, liquidity, risk tolerance and other unique needs.

- Intense credit research is applied within the liquid, high investment grade universe.

- Extensive fundamental, technical and economic analysis is utilized in making investment decisions.