Insights & Observations

Economic, Public Policy, and Fed Developments

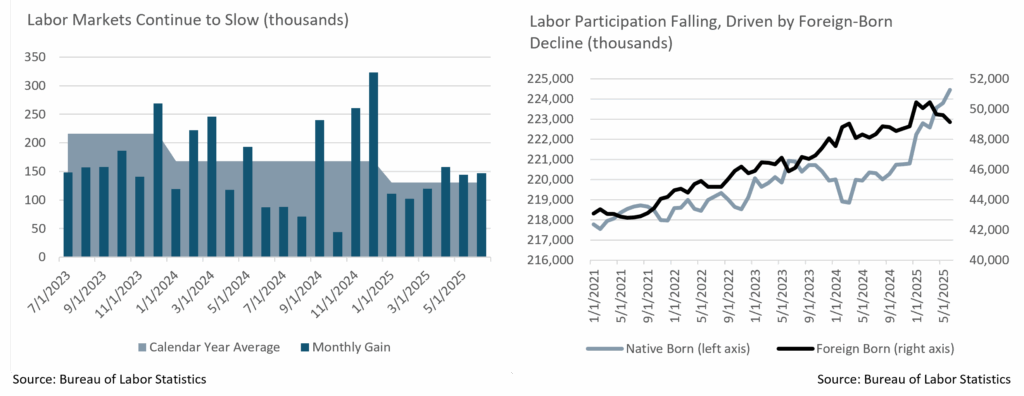

- June was bookended with two labor reports that received very similar, and we believe incorrect, market reactions. Both May’s 139k (revised to 144k) and June’s 147k job gains were objectively weak releases, below the long-term trendline. But the markets treated both as strong due to beating even worse expectations (126k and 106k, respectively). June’s unemployment rate dropped to 4.1%, not due to job creation, but rather falling labor force participation. This was particularly notable in foreign born participation, which had been the backbone of post-pandemic hiring. Meanwhile, private sector hiring was at a standstill in June, with public sector hiring in government and education contributing most of the growth. Markets may have cheered, but this was not a strong report.

- Oddly, this is probably good news for the Fed. The Trump Administration’s trade wars are still far from resolved and likely to reaccelerate as new tariffs are announced. According to the Fed’s Beige book surveys, tariff-related inflation is still to come; businesses have mostly not raised prices yet but expect to do so in the second half of the year. This creates a dilemma for the Fed.

- Their basic problem is this; tariffs can either fuel inflation or depress growth. If consumer spending remains strong, companies can pass along incremental costs, and tariffs lead to higher prices. If consumers won’t pay higher prices, however, then attempts to pass through costs will instead lead to substitution and spending declines. Prices would be largely stable, but consumption and growth would fall. As retail spending is currently weak, and contracted in May, the Fed has legitimate cause to worry about growth. The dilemma, though, is if the Fed starts cutting rates now to stimulate economy, they could fuel inflation by giving consumers the capacity to pay higher prices and turning a demand destruction effect into a price increase one. This in effect gives the Fed a choice between recession if they don’t cut, and stagflation if they do. With post-pandemic inflation fresh in their minds and consumer inflation forward expectations still high, they appear to be more comfortable risking the former.

- For now, the Fed is laser-focused on inflation, choosing to describe the labor market as “not an inflation concern.” This is doubly striking given labor is the other half of their dual mandate. While May and June’s labor reports were weak, they at least took some pressure off by allowing the Fed to continue to focus on beating inflation.

- Meanwhile, after a contentious legislative battle, the “One Big Beautiful Bill Act” narrowly passed Congress and was signed into law. The Administration views this as a growth priority but sweeping Medicaid and SNAP cuts will hit already struggling lower income Americans, and the extension of existing tax cuts is unlikely to be as stimulative as cutting them in the first place was. Longer term, while netted against estimated tariff revenue (if current policies remain) it’s at least no more accretive to national debt than current policy. We are already running a very high current account deficit and eventually this will begin to have implications for the longer part of the Treasury curve.

- Meanwhile, after the US strike on Iran, the Middle East seems to be holding an uneasy peace. After some breakdown to the traditional “flight to quality” trade after the Moody’s downgrade, this geopolitical shock brought a very normal “risk off” reaction, which is welcome. Another flare up remains a risk, however, both in the Middle East and with Treasury yields potentially not responding as they have in years past.

Sources: US Bureau of Labor, Federal Reserve, US Census Bureau

Equity News and Notes

A Look At The Markets

- Stocks rallied throughout June as the S&P 500 gained +5.0% to give the index its first back-to-back monthly gains since September. The Nasdaq gained +6.6%, its 3rd straight monthly gain, and both indexes recorded all-time highs. The DJIA trailed with a +4.3% gain and is still looking for its first all-time high since early December. Within the S&P 500, there was vast sector dispersion with only Technology (+9.7%) and Communication Services (+7.2%) outperforming the overall index. Despite the market’s strength, defensive sectors lagged with Staples (-2.2%) and Real Estate (-0.5%) posting negative returns. Market breadth narrowed considerably in June with the equal-weighted S&P 500 underperforming by 195 bps as larger companies reasserted their dominance.

- On June 27th, the S&P 500 hit its first all-time high (ATH) since February and its fifth of 2025, well off the pace of 57 ATHs in 2024. Remarkably, the index was able to record this new high only 55 trading days after bottoming on April 8th, marking the fastest recovery to a new high after falling -15% or more since WWII. This historic roundtrip follows the pattern of most event-driven bear markets, which tend to be shallower with sharp recoveries, as opposed to economically-driven bear markets which typically fall further and take longer to recover.

- While the S&P 500 enjoyed its 10th best 12-week return of the past 35 years, a collapse in volatility over that same timespan was unparalleled. The VIX fell from over 45 on April 4th to 16.3 on June 27th, the largest decline experienced over the past 35 years. Prior instances of similar price recoveries coinciding with volatility collapses have been accompanied by strong forward returns.

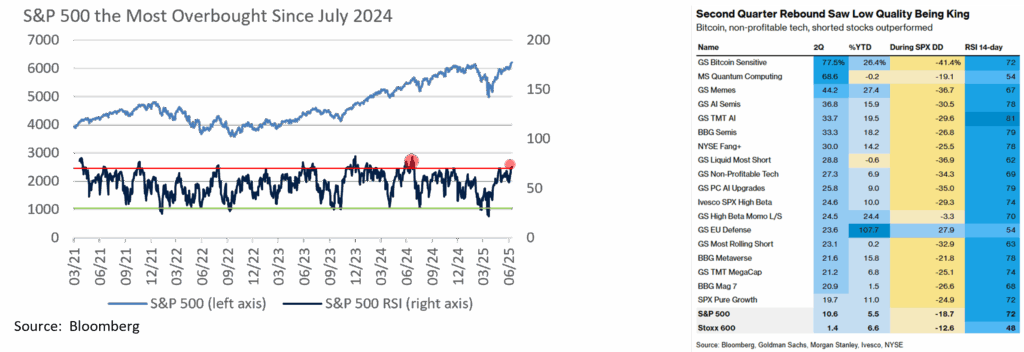

- Q2 started with one of the worst 2-day drops in history before closing +10.6% higher in one of the better quarters we’ve seen over the past 25 years. Investors were in “risk-on” mode as riskier pockets of the market did best in what traders referred to as a “dash for trash.” Baskets perceived to be lower quality such as crypto exposures, retail crowded longs, non-profit tech, high-beta momentum, and the most shorted securities fared best. While we are monitoring an ever-changing leadership, we are encouraged that Financials have joined Tech and Communication Services on the new highs list. With the market arguably as overbought as it has been in nearly a year and stretched from a valuation standpoint, we expect consolidation among lower-quality baskets.

- June’s rally came despite heightened uncertainty around trade, geopolitics, the reconciliation bill, and the Fed, as investors climbed the proverbial “wall of worry.” On trade, while negotiations with China have seemingly improved, the month closed with no official trade deals signed ahead of July 9th, the end of the 90-day pause on reciprocal tariffs. Middle East tensions flared once again with Israel, and later the U.S., bombing nuclear site targets in Iran. Volatility was short-lived as Iran’s counterattack was muted, and the Strait of Hormuz remained open for oil shipments. The GOP’s tax bill passed just before the July 4th holiday, although it remains to be seen how investors digest the impact on US debt and deficits. Lastly, the Fed remained on hold in June with Powell reiterating a patient approach. Nonetheless, FOMC members Waller and Bowman voiced support for a cut as soon as July should inflation continue to ease.

- With the bulls back in charge as the second half of 2025 commences, there remain risks worth watching. The ultimate impact of tariffs on the economy and inflation has not yet been fully felt and the Fed risks a policy mistake the longer they wait. The labor market has shown signs of stress and will need to hold up to keep consumers healthy. Investors will be watching the upcoming Q2 earnings season closely and will look for companies to express a bit more clarity concerning future conditions. We will also be watching trade negotiations as Administration tariff letters go out to individual countries, a process that likely serves to put pressure on US trade partners to agree to more favorable terms. Lastly, a S&P 500 valuation of nearly 22x on a forward P/E basis is historically rich, although markets trading at all-time highs have tended to produce positive forward returns as momentum carries on.

Sources: Bloomberg, FactSet

From the Trading Desk

Municipal Markets

- Municipals extended the bull steepener trade experienced during May with the front end of the curve moving lower as the rates market optimistically priced in Fed action. During June, the 1 to 3-year portion of the curve saw yields decline by 19-22bps and 5-year maturities experienced a yield drop of 17bps. Maturities of 7-years and longer saw the yield rally taper off by 7 to 10bps. 10-year maturities fell by 7bps, while maturities over 10-years saw no yield change, and the long-end of the curve moved slightly higher by 2bps. June saw the spread between 2s and 30s steepen by 21bps, with 12bps of steepening coming from the 2 to 10-year part of the curve. This move in the front-end drove positive price performance.

- Treasury yields exhibited sustained volatility before settling on a downward trend over the second half of the month as municipals closed June richer in the front-end of the curve and cheaper 10-years and out. Specifically, 2, 3 and 5-year AAA municipal/Treasury ratios declined between 1.10-1.96%, while 10 and 30-year ratios widened by 1.56% and 3.42%, respectively. Ratios closed the month at about 70% over 5 years, 77% for 10 years, and just shy of 95% for 30-year issues. The 10-year ratio is approaching the 5-year historical average of 81% while the 30-year ratio has exceeded the 91% 5-year average.

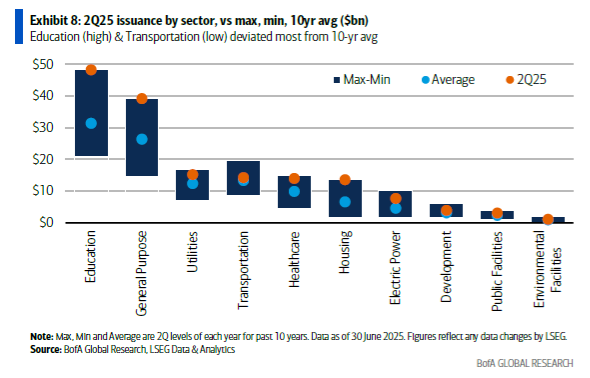

- June sustained this year’s robust issuance with JP Morgan reporting monthly gross new issuance of $57.2B, including taxable and corporate issues. The tax-exempt total of $54.2B marks the 2nd highest month of on record. This brings the YTD tax-exempt total to $256B, a 16% increase vs. 2024’s pace over the same period.

- Municipal fund flows were once again positive at $1.1B for the month according to Barclays, whose analysis noted that these inflows were concentrated primarily in national and long-term funds. On a YTD basis, net fund flows of $10.6B remain robust with ETFs accounting for the majority.

Corporate Markets

- US Investment Grade issuance topped syndicate estimates in June as a last day rush of $8.5B pushed the total to $109.5B. This was the second lowest month of 2025. As was the case in April, new supply was impacted by market volatility. In this case, a softening risk tone and a spike in geopolitical tensions created substantial uncertainty for issuers considering coming to market. Overall, the primary market stands on solid footing as the backdrop for issuers largely remains favorable. Sustained investor demand and falling rates continue to be supportive. July issuance should be strong as it is usually a bank heavy issuance month and may push net new supply well over $100B.

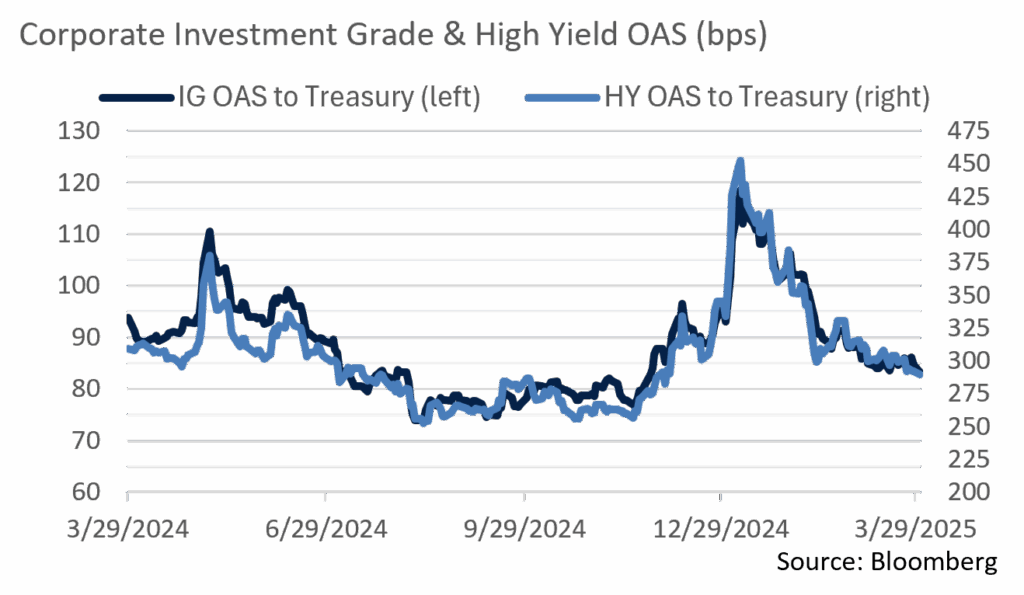

- OAS on the Bloomberg US investment Grade Bond Index has fully recovered from a YTD high of 116bps, rallying to close June at 83bps. This is just 6bps off February’s YTD low. Index performance was +1.87% for the month and is now +4.17% YTD. Intermediate duration has performed better than longer duration YTD, although a recent flattening of the UST curve bolstered longer duration returns in June. This was the first positive month of returns for the index since February, a period marked by a UST rate rally. Over the near term, economic woes and geopolitical tensions could put pressure on credit spreads, although we feel the trend is moving towards finding a bottom.

- High yield risk premiums have decreased significantly with spreads narrowing to the lowest they have been since March and yields moving to levels not seen since December. The 288 OAS on the Bloomberg US HY index is 164 bps below April’s peak. Attractive yields have been pushing investors to chase risk, as evidenced by massive recent inflows into high yield mutual funds. This positive credit backdrop has pushed issuers to the primary market, facilitating the largest IG issuance month of the year at $37.4B. There does not appear to be a near term likelihood that spreads or demand will move in a risk off direction and expect risk assets to perform well going forward.

Sources: MMD, Bloomberg, JP Morgan, Barclay’s, Lipper

Financial Planning Perspectives

Retirement Plan Rollovers

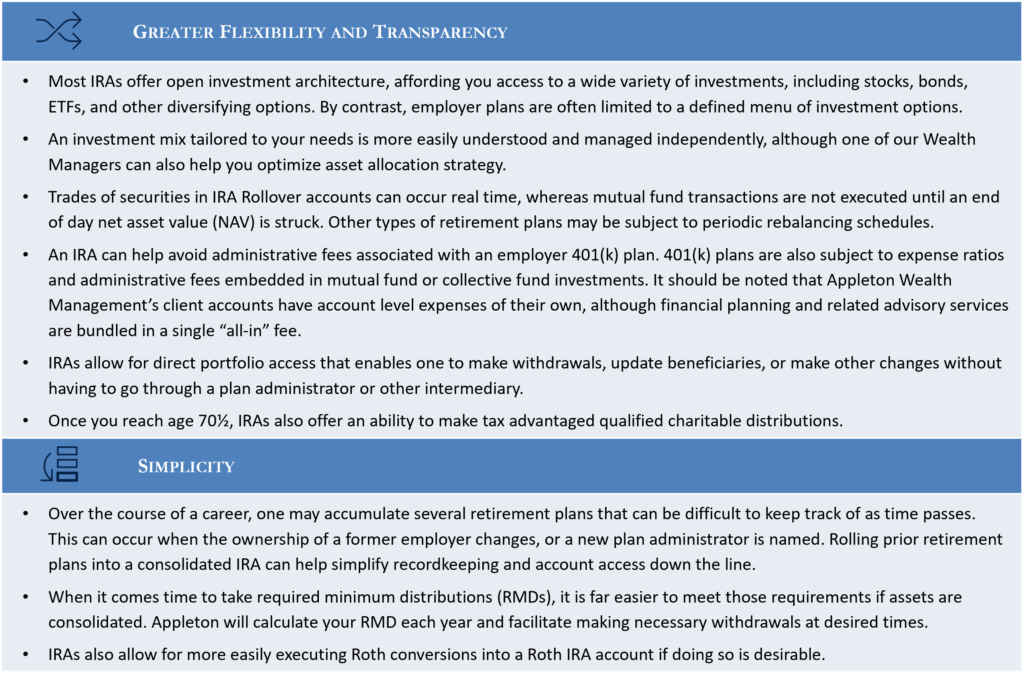

With over four million Americans retiring each year, we encourage clients to review their investment accounts with an eye towards potentially consolidating retirement accounts. In particular, clients may want to consider rolling assets from an employer 401(k) or other retirement plan into an IRA account. Here are a few reasons why this may make sense.

A rollover is not necessarily the right decision for every investor. Employer retirement plans have certain advantages over IRAs. Positive attributes of employer plans include higher contribution limits, potential employer matches, ERISA creditor protection, and an ability to borrow funds. These and other factors must be considered when making an informed decision about whether to roll over assets. Your Wealth Manager can assist you in weighing the pros and cons of consolidating retirement accounts.

It is important to remember that not only 401(k) plans, but also 403(b), 457(b), QRP, and some profit-sharing plans can also be rolled over. Please reach out to your Wealth Manager to discuss considerations of this nature.

Honoring the Life and Legacy of William L. Kingman

It is with great sadness that Appleton Partners announces the passing of William L. Kingman, a former principal of the firm, at age 94. Bill was a beloved colleague, mentor, and Wealth Manager whose leadership was instrumental in our company’s growth and development.

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.