Insights & Observations

Economic, Public Policy, and Fed Developments

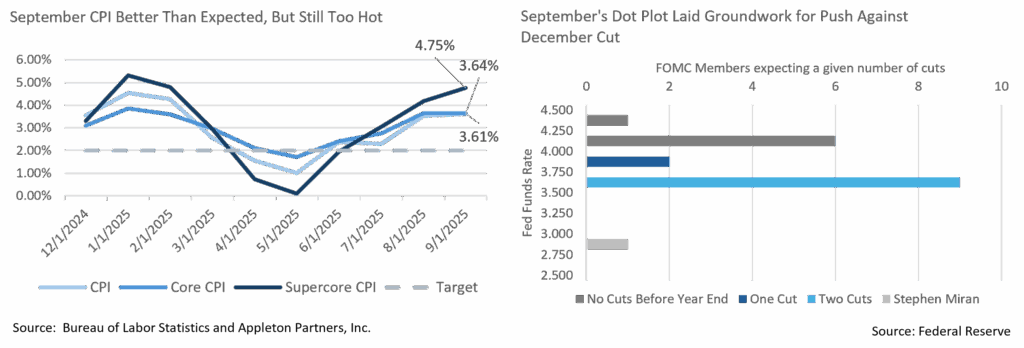

- October was largely a quiet macro month, thanks to the ongoing government shutdown, until the FOMC meeting ended the month with a bang. We thought Chairman Powell might cautiously open the door to a pause after October’s 25bps cut as we still see growing inflation pressures. While Powell described broad support for a cut in October (there were two dissents, newly appointed Stephen Miran favoring deeper cuts, while Jeffrey Schmid favored holding), he indicated the Committee was fiercely divided thereafter. “I always say that we don’t make decisions in advance,” he noted, “but I’m saying something in addition here, that it’s not to be seen as a foregone conclusion, in fact, far from it.”

- Noting the divisions were due to different risk tolerances to the two sides of the Fed’s mandate, we believe Powell subtly indicated growing unease about inflation was at the heart of this divide. We’d previously pointed to the composition of the Fed Dot Plot suggesting a closely divided FOMC as a reason to believe a December cut was not a given. Powell’s Q&A suggested a level of disagreement beyond what we saw in September. We will be watching Fed speakers for signs of further movement in support of a December pause.

- Treasury yields didn’t begin to move materially until midway through the Q&A. Powell began discussing what he initially characterized as a moderately restrictive policy rate. Correcting himself mid-sentence, he clarified, “I would say modestly, other people would say moderately…” This suggests he believes rates are much closer to neutral than the market expected, and that fewer cuts than anticipated will occur. Long term rates ultimately rose about 10bps on the day, based almost entirely on an increase in real yields, as markets began to consider that the current cutting cycle may be nearing its end.

- While not a huge surprise, the Fed also announced the end of “Quantitative Tightening,” their balance sheet roll-off. It will begin in December, a little later than expected, and reinvestment will be in T-Bills, rather than across the entire curve. This is likely to push T-Bill yields down, somewhat steepening the overall curve, and will likely support the Trump Administration’s desire to reduce longer coupon issuance and increase shorter T-Bill issuance. T-Bill yields have been somewhat higher than policy rates would suggest; we expect this to correct as the Fed begins accelerating purchasing.

- After weeks of relative quiet, we also may be nearing the end of the government shutdown. While missed federal paychecks and delays in SNAP payments have been focal points for some time now, a new factor is ACA health exchange open enrollment, which began on 11/1. With Democrats holding out for the continuation of ACA healthcare subsidies, and 2026 enrollment information showing unsubsidized premiums, this pressing issue is going to become much more concrete to voters in coming days. Momentum may be shifting towards a deal.

- We received one government data release in October as the Bureau of Labor Statistics belatedly published September’s CPI report on the 24th. The release was nominally better than expected, coming in a tenth lower than expectations for headline and core, +0.3% and +0.2%, respectively. However, “supercore” inflation, or core services ex- shelter, continues to accelerate, and 3-month annualized rates are rising sharply. Powell has characterized services inflation as fairly well behaved; that may be true in trailing 12-month numbers but is less evident in recent data.

- Another trend worth watching is an acceleration in layoffs. This has been characterized as a “low fire, low hire” economy with little job growth but few staffing reductions. Several big employers, including Amazon and Target, announced sizable layoffs in the last few weeks, however. With an estimated 294k federal staffing reductions from DOGE hitting at the start of October, there is risk that the “curious balance” of the labor market could shift.

Sources: Bureau of Labor Statistics, Federal Reserve, and Bloomberg

Equity News and Notes

A Look At The Markets

- Seasonal weakness failed to materialize in October as each of the major domestic indices closed higher. The S&P 500 pushed its monthly winning streak to 6, making 8 new all-time highs (ATH) and gaining +2.3% to bring its YTD total return to +17.5%. The Nasdaq outperformed, up +4.7% (+23.5% YTD), as the Technology sector was the month’s top performer at +6.2%. Healthcare and Consumer Discretion were the only other sectors to outpace the overall index, while cyclicals and defensives closed mostly lower. Both the DJIA and Russell 2000 made fresh ATHs in October but continue to trail the S&P 500 on a YTD basis (+13.3% and +12.4%, respectively)

- One of the bigger stock market dynamics at play is a deterioration in breadth, as last month’s gains were largely concentrated in larger cap names. The equally-weighted S&P 500 (RSP) trailed the cap-weighted index (SPX) by 3.2%, closing -0.9% lower on the month. The RSP lagged the SPX by 0.5% over four straight trading days, something never seen in the history of the RSP (2003). October 28th also marked a first for the SPX, as the index closed +0.23% higher despite 398 stocks declining versus only 104 advances. These breadth readings are indicative of concentration risk in the index, a theme we’ve touched on many times in this space. Nonetheless, the RSP made its own all-time high in late October and historically has rolled over well ahead of the official index. For now, it is not a strong signal, but something demanding attention in the days ahead.

- Looking at fundamentals, the Q3 earnings season has provided a tailwind for stocks. With 64% of the S&P 500 having reported, a historically strong 83% have beaten consensus earnings estimates by an average margin of 5.3%. That’s lifted the blended earnings growth rate to +10.7%, well ahead of the September 30 estimate of +7.9%. Should this growth rate hold, it would mark the 4th straight quarter of double-digit growth. Top line results have also been impressive with 79% of companies beating revenue estimates by an average margin of +2.2% to bring the blended growth rate up to +7.9%. Net profit margins also continue to hold in well, expanding to +12.9% (5-year average: +12.1%) despite concerns over tariffs and rising costs. This earnings season has been welcomed by the bulls for multiple reasons. Stock prices tend to follow earnings over the long-term, and earnings growth will be necessary to justify today’s elevated valuations. We also feel a recession is unlikely given this level of corporate profit growth.

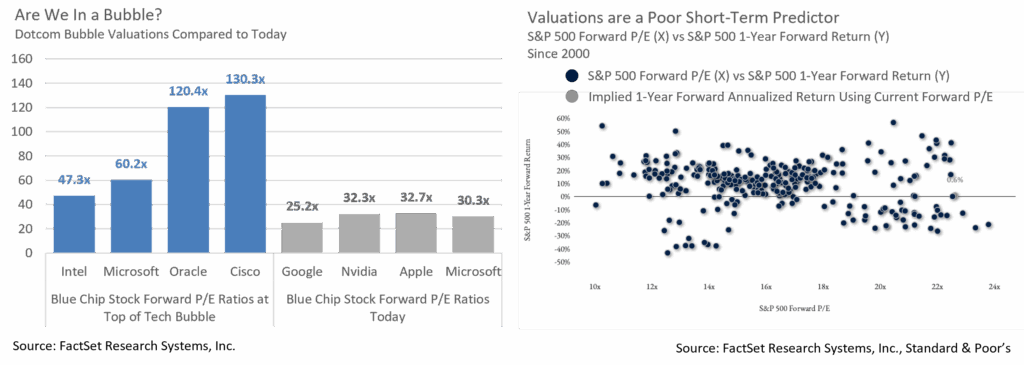

- Many investors are growing increasingly concerned about valuations, or even “bubbles”, as the S&P 500 recently traded near 23x forward earnings. You will get no argument here that stocks are cheap, and we too feel that pockets of the market are frothy. But we caution against making buy/sell decisions solely based on P/E multiples or comparing the market to technology bubble days quite yet. As shown below, P/E multiples are a poor predictor of short-term returns, and we currently view it more as stocks having a narrower margin for error.

- The market shook off several macro concerns over the course of October as AI optimism, easing monetary policy, and strong corporate profit results further fueled an historic rally off the April lows. The ongoing government shutdown delayed most economic data releases, limiting clarity into the health of the labor market. We believe the shutdown’s lasting impact will be limited, but the longer it carries on, the greater the odds of an economic soft patch.

- October also faced a short-lived credit scare after fraudulent loans were discovered at two small regional banks, and a brief escalation of trade tensions with China which ended with a détente between Trump and Xi late in the month. Stocks were also pressured when the Fed Chairman pushed back on the idea that an additional rate cut in December was a foregone conclusion. While the shutdown and path of monetary policy are front of mind as we head into November, the stock market typically does well over the final 2 months of the year, particularly after posting strong YTD gains.

Sources: Bloomberg, FactSet

From the Trading Desk

Municipal Markets

- October saw the continuation of the curve flattening that began in the prior month. The front end repriced higher in yield, while maturities 7 years and longer saw strong investor demand and an overall yield rally that peaked in 12-15 years. Performance was strong with 15 and 20-year maturities topping out at over 2%, outshining other spots across the curve. The short end was a laggard with mildly negative monthly returns.

- The 1 to 3-year part of the AAA curve saw yields increase up to 18bps, while 5-year maturities saw a more modest yield increase of 6bps. Strong demand for maturities greater than 6 years pushed yields lower by 4 to 24bps. The most significant rally, however, occurred 12 years and out on the curve, where yields closed the month lower by 22 to 25bps, rewarding duration.

- A net effect of these dynamics was that the slope of the curve ground lower, largely on par with the record move we saw in September. Our bell-shaped curve positioning and emphasis on the longer end of our intermediate strategy range is paying dividends, as many investors have added duration after selling short paper, a repositioning that has aggressively bid up longer maturities. These are trades we worked on throughout the summer after the curve reached historic steepness.

- According to JP Morgan, gross issuance totaled $59B, modestly lower than October 2024’s figures, while tax-exempt supply came in at $49.5B. The latter, while slower than the same period last year, pushed 2025 supply ahead of last year’s pace by 11%. This brings YTD gross supply to $484B, while the tax-exempt issuance total is $442B. As supply has been waning off a previously aggressive path, this might prove to be a supportive sign for municipals during November, a month in which estimated redemptions of more than $30B are expected, and activity around the Thanksgiving holiday is typically subdued.

Corporate Markets

- The primary market ended the month of October with a bang, as the year’s largest deal came just one day after the much-anticipated FOMC rate decision. Whie the Fed’s action didn’t spook the market, a $30B bond offering from META surprised participants, although they did not shy away. The deal amassed $125B in orders, and spreads tightened significantly from initial price talk. The deal with the fifth largest on record, falling just behind Pfizer’s $31B offering on 05/16/23. After a very slow start, this deal propelled the month into the record books as the largest October in history with $131.9B issued. While November is expected to bring $120B of new supply, more than that could end up being issued if market conditions remain favorable.

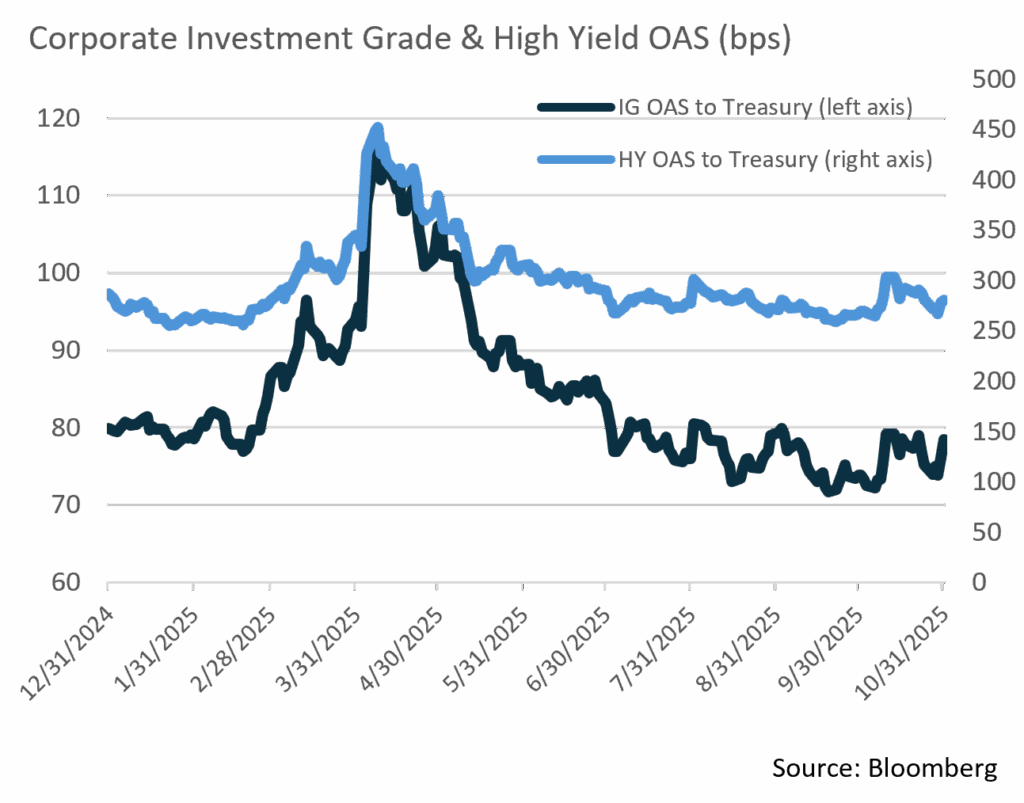

- Given such high levels of new supply, one might be concerned that buyer fatigue would begin to creep into the market. That has yet to be the case as solid technicals have allowed spreads to remain steady. In fact, the 78 bps OAS print on the Bloomberg US Corporate Index is 5bps lower than where July began. Over that timeframe the market has moved just 10bps in either direction, averaging an OAS of 77bps. The FOMC’s decision to cut the Federal Funds Rate and to roll back Quantitative Tightening is good for the momentum of credit spreads. With another cut in December hardly a done deal, we feel that IG credit spreads will remain in a narrow band to close out the year.

- According to Lipper, Short and Intermediate fund flows remained strong in October. The $11.04B of net new assets gathered by these funds has been a strong technical contributor to spread stability and new issuance demand. High Yield Fund flows were modestly positive at +$1.12B.

Sources: Bloomberg, JP Morgan, and Lipper

Financial Planning Perspectives

Modernizing Payments To and From America’s Bank Account

In March, the White House issued Executive Order 14247, “Modernizing Payments To and From America’s Bank Account” that phases out paper checks in favor of electronic payments beginning on September 30, 2025. This initiative encompasses estimated tax payments, social security benefits, tax refund checks, and more. At present, about 95% of federal payments are made electronically, so while this affects only a small portion of payments, we want to ensure that our clients understand alternative ways to send or receive funds.

Payments to the IRS:

- •IRS Direct Pay – issues payments directly from your bank account at no charge. For more information, please visit: https://www.irs.gov/payments/direct-pay-with-bank-account

- •Electronic Federal Tax Payment System (EFTPS) – available for use by individuals and businesses. Additional details are available at: https://www.irs.gov/payments/eftps-the-electronic-federal-tax-payment-system

- •IRS2GoApp – a mobile app used to make secure payments. For more information, please visit: https://www.irs.gov/help/irs2goapp

- •Debit or Credit Cards

Refunds or Federal benefit payments:

- Direct Deposit – this can be arranged by providing your bank’s routing number and your bank account information when filing a tax return. This can be accessed by going to GoDirect.gov.

- Mobile Apps and Prepaid Cards (Direct Express Card) – they can be used if you have submitted proper bank account information.

There are few exceptions to these electronic payment requirements. They include individuals without access to banking services, emergency payments, and national security circumstances where non-EFT transactions are needed.

The objectives of these new requirements are to:

- Realize processing efficiencies, including IRS and Treasury Department cost reductions

- Speed up customer receipt of tax refunds

- Fight check washing and other crimes by utilizing electronic channels

- Increase overall federal payment security

Additional information can be found on the websites referenced above, or by speaking with your Wealth Manager. Please reach out with any questions on this issue or other financial planning needs. Best wishes for the upcoming holiday season!

Source: https://www.irs.gov/newsroom/modernizing-payments-to-and-from-americas-bank-account, https://www.mymoney.gov/federalpayments, https://www.ssa.gov/news/en/advocates/2025-09-10.html

At Appleton Wealth Management, we take great pride in the financial planning services provided to our clients. Is there someone you care about who might benefit from working with us, but you’re unsure how to make the introduction?

If so, please let us know. We are happy to help.

Please contact your Wealth Manager or Jim O’Neil, Managing Director

617-338-0700 x775 | [email protected] | www.appletonpartners.com

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen, or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.