Insights & Observations

Economic, Public Policy, and Fed Developments

- Most of the interesting market news from January might be best described as changes to the market backdrop, rather than foreground action. While a lot of it may not have been immediately market moving, we believe some of these events will play out in important ways as the year goes on.

- The largest was the surprise announcement of a Department of Justice investigation into Fed Chair Jerome Powell over ongoing Federal Reserve renovations. Trump has complained about cost overruns here in the past, but this represented a significant escalation, and one for the first time Powell suggested was intended to influence rate policy. Bipartisan outcry was immediate, and the head of the Senate Banking committee, Sen. Thom Tillis (R-NC), vowed to block hearings on any Fed appointees until this matter was resolved. In practice, this could leave Powell as Acting Chair beyond May.”

- Meanwhile, Trump announced federal housing agencies Fannie Mae and Freddie Mac would use $200B in cash on hand to purchase mortgages. This was intended to drive down mortgage rates as part of a broader “affordability” push before the midterms, in what is effectively “QE-like” market activity. While the immediate impact on borrowing costs was modest, we expect the Administration to continue to seek ways to inject monetary stimulus independent of the Federal Reserve.

- This is interesting, because at month-end Trump finally announced his pick to replace Chair Powell when his term ends in May. Kevin Warsh is considered a relative hawk and known as a vocal proponent of shrinking the Fed’s balance sheet, which would in effect be quantitative tightening. Market reaction to Warsh’s nomination suggested some relief for a relatively mainstream choice, with the dollar strengthening on the news. Senator Tillis was complimentary to Warsh but reiterated the Senate Banking Committee will not hold confirmation hearings while Powell is under investigation.

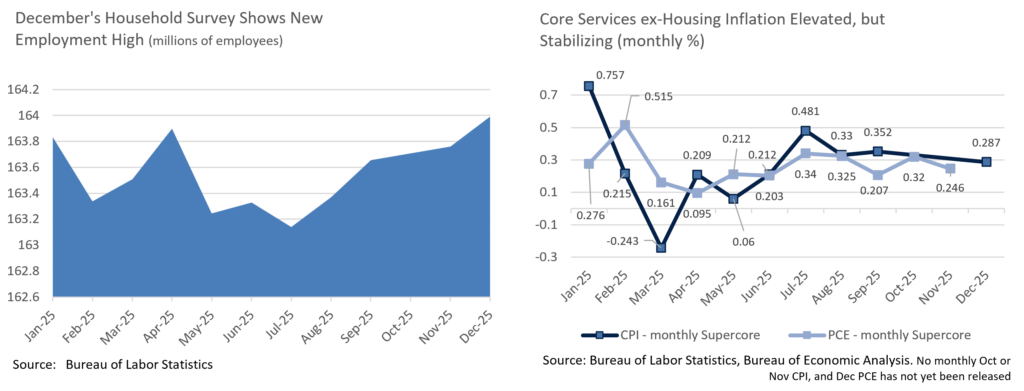

- There were several pieces of economic news last month that we found encouraging as well. First, the Fed’s Beige Book survey showed economic activity broadly strengthened, a clear improvement from the last several surveys. Second, while CPI continues to be impacted by the missed October shelter cost survey and the December shelter cost increase of 0.405% is a little concerning, the long-elevated “supercore” CPI (excludes shelter) is now trending downwards, and is converging with the high, but rangebound PCE “supercore” which has been running at a monthly rate consistent with annualized 3% inflation. We note that the January PPI inflation shows evidence of margin expansion, and while it’s too early to say if this is falling input or rising output prices, the latter would risk spilling into consumer price measures and should be watched. On balance, inflation data appears to be moving in the right direction, though for the last several years annual adjustments and rebalancing has led to January spikes, and we see risk of a continuation.

- Finally, we see some signs of stabilization in the labor markets. While nonfarm payrolls missed expectations, the unemployment rate unexpectedly dropped two tenths to 4.4% on the back of a much larger jobs gain, and a drop in unemployed workers, in the Household Survey. Giving us added confidence here is the Household survey’s total employed figure, which after a period of weakness in the summer and fall, has been in an uptrend and finally exceeded April’s 2025 high-water mark.

- All told, we believe Chair Powell was right to conclude that while there were still risks to both sides of the Fed’s dual mandate, they had diminished somewhat and were back in balance. We expect the Fed to remain on hold for the foreseeable future. Further reductions in the second half of the year are possible, but we believe the Fed will need data to paint a convincing case for cuts before they act.

Sources: Federal Reserve, Bureau of Labor Statistics, and Bureau of Economic Analysis

From the Trading Desk

Municipal Markets

- Municipals were off to the races in the New Year as January saw strong price performance, primarily out to 15 years. This occurred against a backdrop of supply that seemingly could not keep up with the demand from significant inflows and reinvestment. Rates rallied in a descending fashion (i.e. the short end outperformed) and the curve steepened. Specifically, the spread between 2s and 30s steepened by 26bps, while 2s to 10s and 10s to 15s steepened by 8bps and 11bps, respectively.

- The curve from 7-years and in saw absolute yields move significantly lower, specifically by 28bps for 1-year issues, 20bps for 3-years and 14 for 7-years. 10 to 15-year maturities moved lower, notably by 13bps in 10-years, while the 20-year spot increased 4bps. The long end (25 to 30-years) saw yields push higher by about 4 – 5bps, contributing to a steeper curve.

- Municipal ratios followed a similar pattern as ratios out to 10-years fell, with 20-years and longer staying relatively flat. Ratios out to 3 years tightened by about 5-7%, settling at 61%, while 5- and 7-year ratios dropped by 5% to close the month just shy of 60%. The 10-year maturity ended at 62%.

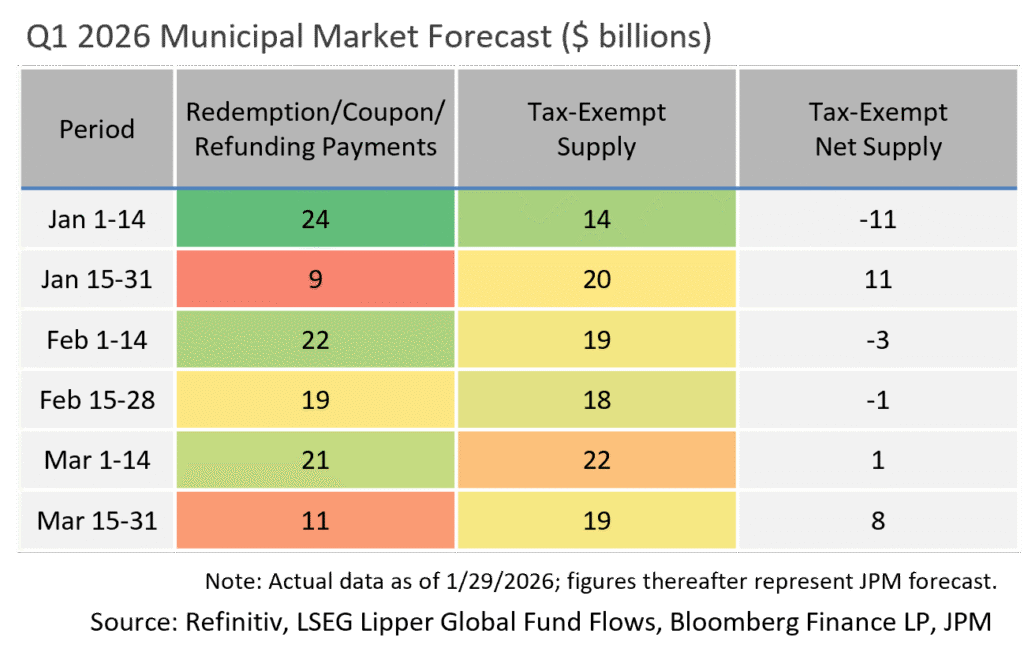

- According to JP Morgan, tax-exempt issuance in January totaled $34B, $1B lower than last year’s record. Over the month, gross issuance hit $35B, just below the $37B seen in the prior January.

- Municipal fund flows surged in January with net subscriptions totaling $6.4B based on data reported weekly to Lipper. JP Morgan estimates that municipal inflows could reach $13B once monthly reporting funds are factored in, which would be one of the highest months on record since Lipper started tracking in 1992.

- Market technicals are setting up for a constructive February, aided by $40B of reinvested principal and interest. Of note, this would be a record for February reinvestment, surpassing the prior peak of $37.5B recorded in 2017.

Corporate Markets

- UST yields moved modestly higher in January with a slight tilt toward curve flattening. The 10Yr bond rose 7bps to 4.24% after hitting a YTD high of 4.29% on January 20th, a level not reached since last August. We see a resistance level in the 4.25% range. Rates down the curve followed the same path with 2 and 3Yr issues higher by 5bps to 3.53% and 3.59%, respectively. The 1Yr remains the lowest yielding point on the curve at 3.48%. In our view, the 10Yr will remain range bond in the near term with a downward bias given uncertainty swirling around the markets.

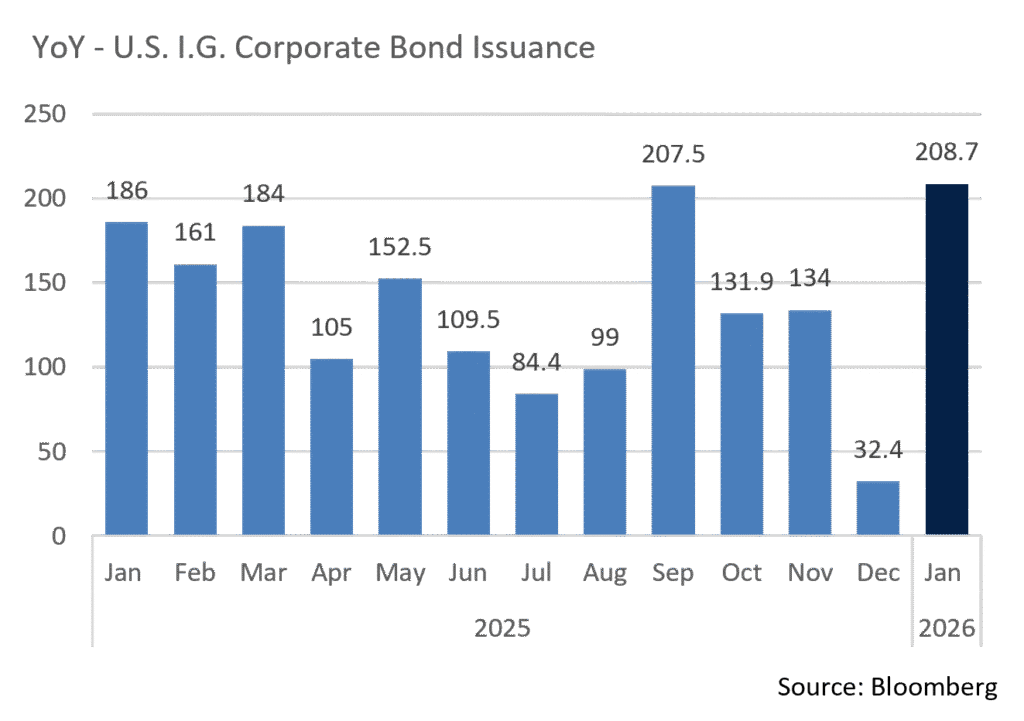

- January’s $208.7B of new debt brought by issuers was the largest monthly total since September’s $207.4B. It was also the 5th largest month on record and 12% higher than this same time last year. It is worth noting that the Financial sector accounted for 56% of last month’s issuance led by the US “Big Six” banks. The most notable deal was Goldman Sachs, who brought $16B of new debt mid-month, the largest investment grade Wall Street bank offering ever. As with others, management capitalized on attractive funding cost, strong investor demand, and a still solid economy. 2026 is expected to be a record setting year for issuance and, so far, things are moving in that direction. As long as the technical backdrop remains strong, the $190B expected to come in February should be realized.

- Investment Grade and High Yield spreads remain tight and feverish demand is keeping valuations strong. The Bloomberg US IG Credit Index OAS began the year at 78bps before moving higher by 5bps at month’s end. $15B of net fund flows (as per Lipper) bolstered demand, the lion’s share of which went into Short and Intermediate funds. We anticipate a continuation of tight, range-bound Investment Grade spreads over the next few months. However, a risk bifurcation became evident in January, as High Yield funds saw outflows of $869.7M.

Sources: Bloomberg, Bond Buyer, Barclays, JP Morgan, and Lipper Inc.

Public Sector Watch

U.S Census Data

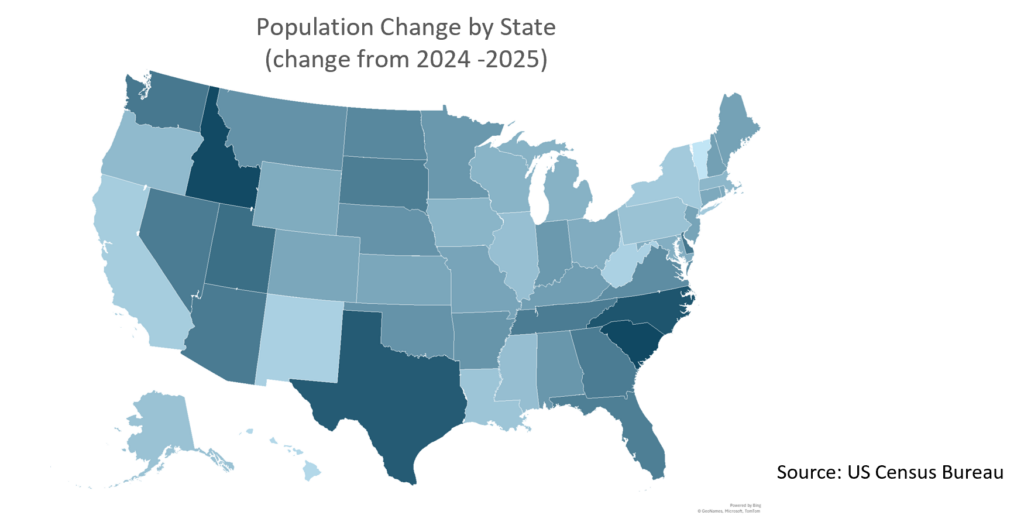

- Census data indicates that U.S. population growth slowed in 2025, increasing by just ~1.8 million people, or 0.5%, YoY to reach 341.8 million. That is down from +1% in the prior year, and a decline from a 0.7% average annual growth rate from 2010 – 2020.

- Births and deaths changed only slightly from the preceding 12-month period. A more significant factor in the change was net immigration. The census estimated 1.3 million net arrivals in the most recent measured year, down 54% from the preceding 12 months, a period when migration to the U.S. was at a historically high rate.

- The data highlights trends in various states and regions. The South was the fastest growing region, sustaining a recent trend. More surprisingly, the Midwest posted slightly positive net migration for the first time this decade. The Midwest was the only region where all states gained population. The West and Northeast experienced net negative domestic migration, although each of the four regions within the U.S. gained population with the help of immigration.

- Only five states experienced a population loss – Vermont, Hawaii, West Virginia, New Mexico and California. California has seen net negative domestic migration in years prior, although in 2025 an international immigration decline was enough to tip the state into a slight population loss.

- Population trends are an important factor in municipal credit research as significant changes can impact or highlight underlying economic trends. Population changes drive the size and stability of the tax base, demand for services, and long-term economic vitality.

Sanctuary Cities/Jurisdictions

- President Trump recently made threats to “sanctuary jurisdictions,” stating he would halt federal funding if they failed to cooperate with federal immigration enforcement. The Federal government has not stated what they expect to happen to these “sanctuary cities,” but based on past actions, there will be further attempts to withhold federal funding. In our opinion, the Administration is unlikely to be successful in disrupting funding or negatively impacting credit quality.

- Should funding be interrupted, it would still likely be manageable for stronger state and local governments, as the Federal funding that could be cut is likely a small percentage of these municipalities’ annual budgets and can be covered with reserves, expense cuts, or revenue increases.

- In the first Trump Administration, an Executive Order to eliminate Department of Justice funding for municipalities that did not comply with federal immigration enforcement requests was struck down by the courts. The most recent attempt in this Administration’s second term was also recently blocked by a federal judge.

- Courts have ruled on multiple occasions that the executive branch is prohibited from withholding funds to state and local governments as a tactic to leverage public policy, and that any actions to withhold those funds requires Congressional approval. Given a very narrow GOP majority in Congress and competing legislative priorities, we believe Congressional action on “sanctuary city” actions is currently unlikely.

- The fact pattern points to a low probability of Federal funding being interrupted for “sanctuary cities,” and even if the Administration is successful at interrupting, delaying or cutting such funding, Appleton invests in high-quality local governments with diverse revenue streams and ample balance sheets, attributes that provide a considerable margin of credit cushion.

Sources: U.S. Census Bureau, S&P, JP Morgan and BofA

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Not all products listed are available on every platform and certain strategies may not be available to all investors. Financial professionals should contact their home offices. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen, or experience. Investments and insurance products are not FDIC or any other government agency insured, are not bank guaranteed, and may lose value.