Insights & Observations

Economic, Public Policy, and Fed Developments

- For some time now our view has been that the labor markets are somewhat stronger and progress lowering inflation is somewhat weaker than the market consensus holds. Nothing has fundamentally changed this view, but quite a lot happened in February that we think deserves attention.

- As expected, in a 6-3 decision, the Supreme Court found the Trump Administration’s use of the International Emergency Economic Policies Act to apply tariffs without Congressional review unconstitutional (notably, the dissents were focused more on disruption than legal questions). Trump wasted little time turning to a new avenue, applying tariffs under Section 122, a legally vetted mechanism that allows him to do so up to 15% for up to 150 days without Congressional action. We believe exact rates are less important than the point at which companies can consider tariffs “settled” and begin to plan around them; this adds significant uncertainty.

- In the short term, with rebates possible but ongoing tariff levels only slightly lower, there was not much movement in longer rates. We are monitoring discussion around rebates, which are likely, though the possibility of Congress authorizing payments to American citizens (without also a directive to not rebate importing companies) remains a risk, as this would double the budgetary impact of the Court decision and could impact longer rates.

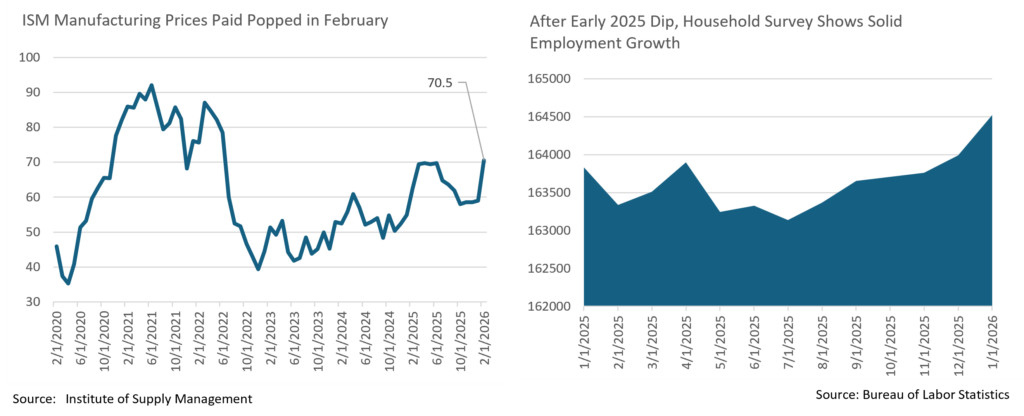

- January’s Nonfarm Payrolls report had little not to like; employment growth doubled expectations, at 130k, the unemployment rate fell a tenth and nearly rounded to a two tenths improvement, in the Household survey both participation and employment rose substantially, sustaining strong growth since mid-summer, and earnings growth was respectable. Expectations for February remain low, with a Bloomberg consensus of 59k and an unchanged unemployment rate of 4.3%. All the same, a market consensus that the Fed needs to lower rates to support the labor market is hard to square with what looks like healthy labor conditions.

- Markets positively reacted to the January CPI report, despite our misgivings (our February white paper discussed this issue). Subsequent data has done a good job demonstrating why we are concerned. The first Fed Beige Book of the year showed companies that hadn’t yet passed along tariffs were starting to capitulate and raise prices. For nearly a year now we’ve been concerned that uncertainty around tariff policy was stretching this pass-thru process out. A hot PPI report with a large contribution from trade services (implying margin expansion, we believe from compressed levels where tariffs were being absorbed), and an unexpected surge in the Prices Paid component of the ISM Manufacturing index to the highest level since 2022 gave credence to this survey. We continue to expect a reacceleration of inflation in the first half of 2026.

- Joint US and Israeli strikes on Iran were the final unexpected macro development bookending February. The initial rate move was down, to nearly 3.92% on the 10Yr at the lows, but interestingly as it became clearer that this conflict could last at least several weeks, rates reversed. As of morning trading on Tuesday, March 3rd, the 10Yr was back over 4.10%. Some of this move is a market reaction to the ISM Prices data, but we also suspect that the traditional “flight to quality” may have been overpowered by a combination of concerns over the war’s impact on inflation, and the potential for larger US deficits if military action is prolonged.

Sources: Bloomberg, Bureau of Labor Statistics, Institute of Supply Management, the Federal Reserve

From the Trading Desk

Municipal Markets

- Municipal performance remained strong in February, buoyed by significant intra-month redemptions (est. at >$40B) and fund subscriptions.

- Municipal yields rallied in a largely parallel fashion with the most significant move in the 15-year spot on the curve. The 2s-30s curve went net steeper by 3bps but effectively twisted. The slope inside of 10 years steepened by 1-3bps, while 10s-15s flattened by 8bps as more market participants pushed out the curve in search of value.

- With regards to absolute yield moves, 5-year issues and shorter fell by anywhere from 14-to-16bps. The 7- to-12-year maturities moved lower in a similar fashion, notably by 11-13bps, while the 15-year spot experienced the most aggressive move down in yield, declining by 19bps. The long end (25- to-30-years) finished the month lower by 16bps and 12bps, respectively.

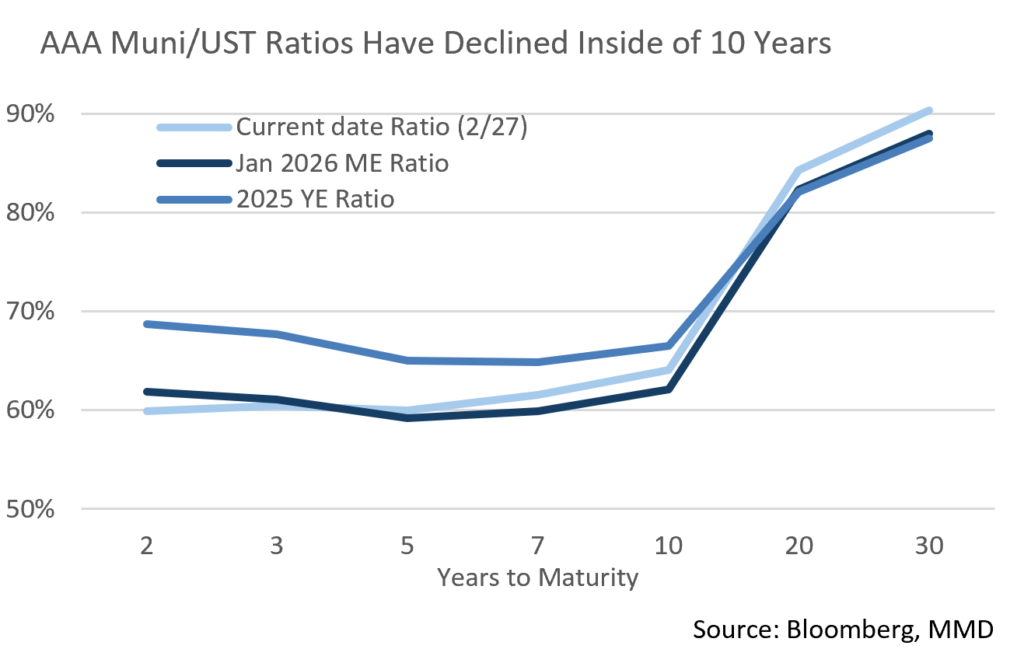

- Municipal ratio moves were more muted after the significant strength of the prior month. Ratios in the 2- and 3-year range moved slightly tighter by 2% and 0.66%, respectively, while all maturity points of 5-years and longer saw slightly cheaper ratios, within a range of 0.79-2.32%. The month closed with the 3-year ratio at 60.4%, 5-year at 59.9%, and the 10-year settled at 64%. On the long end, the 30-year maturity widened to 90.3%.

- According to JP Morgan, February tax-exempt issuance totaled $40B. From a relative standpoint, long-term tax-exempt supply set a new high-water mark in February, besting the prior records of $37B in 2007 and $36B for 2025.

- Market technicals should weaken in March in line with seasonal expectations, with redemption capital estimated at $32B vs. estimated supply of $41B. This could loosen up tight ratios and unlock opportunities for tax-exempt investors.

Corporate Markets

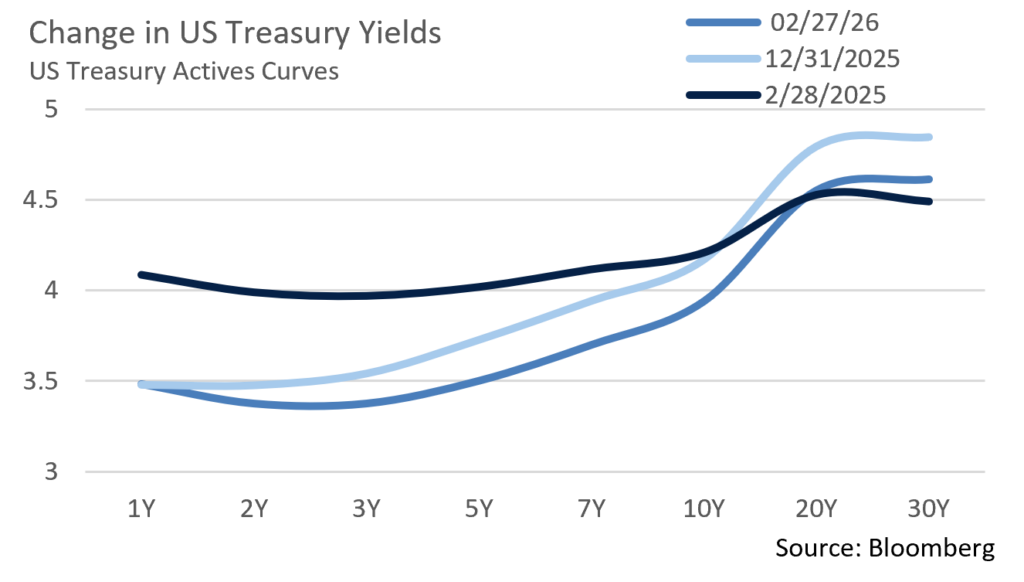

- Treasury yields fell significantly in February, largely driven by a month-end rally into safe havens. The curve shifted down in a parallel manner that retained prevailing steepness over 2 to 20-year maturities. However, this move deepened a yield trough between very short issues through the 7-year part of the curve. For example, the 7-year benchmark dropped 31bps to 3.71%, a level that was only 3bps higher than the 4-month T-Bill which did not move in yield. Benchmark 10-year, 20-year, and 30-year bonds all moved lower by 26 to 29bps with the 10-year closing at 3.95%.

- The economic picture, particularly inflation pressures exacerbated by the US and Israeli attacks on Iran, may keep the Federal Reserve on hold for the time being. Rising global tensions could produce a further “risk-off” move towards assets such as Treasuries, placing downward pressure on yields.

- After tightening to begin the year, US Investment Grade credit spreads retreated in February. A 73bps OAS spread on the Bloomberg US IG Corporate Index rose to 84 bps by month’s end, the highest level so far in 2026. While the Index produced positive returns, the effects of widening created negative excess returns vs. Treasuries. Global market uncertainly is to blame here, not credit concerns. Demand for IG credit remains strong, and we feel that modest widening of credit spreads is healthy given the relative tightness the market has long been experiencing. Over the near term, additional widening is likely although we expect investor demand to dampen the magnitude of this move.

- The Investment Grade primary market remains robust and the landscape for issuers is still attractive. Concession levels are still very low and almost non-existent for high quality deals. The $190.9B of new debt issued MTD is right on the target set by the syndicate. That included a $20B jumbo deal brought late in the month and a similar-sized deal in January. Expectations for the March calendar are high at $230B although war in the Middle East has already left issues on the sidelines while more offerings may be delayed in the weeks to come. At this point, YTD expectations for $1.85T remain in place.

Sources: Bloomberg, Bond Buyer, Barclays, JP Morgan, and Lipper Inc.

Public Sector Watch

Chicago Credit Challenges Continue

- The City of Chicago has faced financial challenges for decades and has had difficulty achieving structurally balanced budgets amid chronic reliance on one-time fixes and optimistic revenue outlooks.

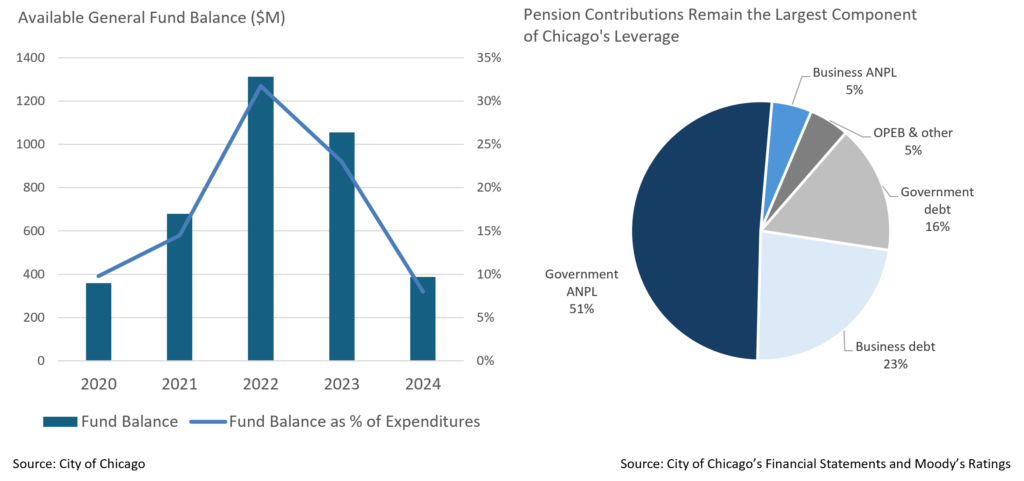

- In FY 2026, the City is facing a budget deficit of close to $1.2 billion, or about 20% of the general fund budget, and outyear budget deficits are estimated at approximately $1.2B, for both FY27 and FY28.

- There is widespread disagreement among leaders concerning the best way to close the current year deficit. The City Council rejected key parts of Mayor Brandon Johnson’s proposal and, in an unprecedented move, passed an alternative budget without the Mayor’s signature; the first time a budget was passed in this manner in 40 years.

- Chicago’s budget continues to rely on several unsustainable measures. It eliminates a controversial corporate head tax that would have raised $100 million and instead includes a patchwork of several uncertain sources to fund rising expenses such as a percentage point increase in the personal property lease transaction tax rate, new taxes on sports betting, and plans to securitize and sell receivables, among others. While the City can implement property tax increases under home rule, they do not appear to have political support.

- Chicago is seeking to sell about $1 billion of debt from securitization of uncollected debt owed to the City despite warnings from finance officials that investor appetite is shaky and therefore would likely come at a high cost.

- Mayor Johnson opposed the move, arguing it would hurt taxpayers that could become victims to debt collection firms. Such a move is considered fiscally imprudent and a sign of a challenged credit.

- Chicago does have several positive attributes, such as its position as the economic engine for the Midwest region, an extensive transportation infrastructure network supporting ample job opportunities, and a diverse employment base. However, the City’s governance practices are weak, and conflicts relating to spending, tax increases, and other political challenges have led to an inability to produce timely and structurally sound budgets.

- Chicago also remains pressured by its large and growing pension burden, with recent sizable contributions still below actuarially determined amounts. These ongoing budget challenges are driven by an inability or unwillingness to produce the sustained revenue sources needed to structurally balance operations. This will, in our view, continue to stress the City’s credit profile, supporting Appleton’s longstanding PASS recommendation on the City’s General Obligation bonds.

Sources: City of Chicago, Moody’s, S&P, JP Morgan, Bank of America

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Not all products listed are available on every platform and certain strategies may not be available to all investors. Financial professionals should contact their home offices. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen, or experience. Investments and insurance products are not FDIC or any other government agency insured, are not bank guaranteed, and may lose value.