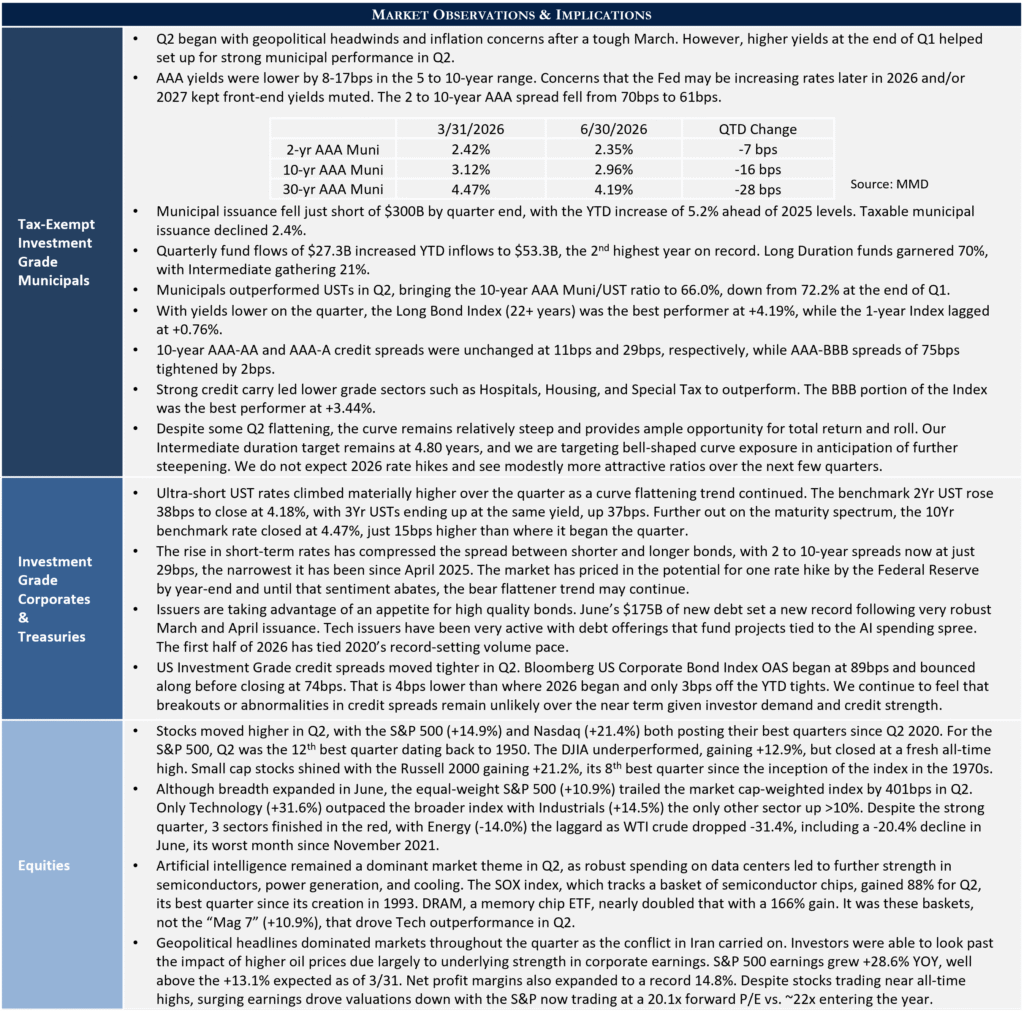

“The enduring strength of the 60/40 portfolio suggests that investors looking to build diversified portfolios don’t necessarily need to venture too far beyond a basic mix of larger-cap stocks and high-quality bonds.”

(Morningstar, April 2026)

Human nature often drives us to project forward what has most recently occurred, a phenomenon known as recency bias. Placing too much emphasis on the immediate past can distort our perception of the future. Behavioral finance tendencies of this nature are pervasive, and the last several years offer a good example.

Balanced strategies have long been a mainstay of asset allocation, a construct supported by the conventional wisdom of diversification. Confidence in this approach was severely tested though from 2022 to 2024 as traditionally negative correlations between stocks and investment-grade bonds turned positive. When bonds failed to buffer equity exposure, and both asset classes produced negative returns, many advisors soured on the concept.

What Went Wrong?

Before defending the methodology, let’s briefly look at why it has not performed as expected over much of the 2020s. COVID-related supply chain shocks coupled with aggressive federal stimulus sent inflation soaring early in that period, which in turn triggered the most aggressive interest rate hikes in decades in 2022 and 2023. As investors grappled with recession fears and spiking interest rates, stock and bond prices simultaneously declined, causing their correlation to turn positive. For a brief time this spring, a similar dynamic played out as the Iran War caused a surge in geopolitical risk and energy prices, along with renewed inflation concerns. Fortunately, fears have moderated, and markets, while volatile, are holding up well, yet asset allocation questions linger. Is the old model becoming dated?

An Abridged Explanation of Diversification

A key tenet of portfolio theory is that assuming greater risk creates the potential for greater return. However, aggregating the risk and return characteristics of underlying investments is not simple arithmetic. Within an asset allocation plan, combining investments with low or negative correlation can reduce overall portfolio risk as these assets are unlikely to experience downturns at the same time. By contrast, the expected return of the entire portfolio is derived from the weighted average of each asset class’s expected return. Therefore, a risk-related benefit of high-grade bonds in a diversified portfolio lies in how they interact with other exposures.

Why Take a Balanced Approach?

Readers of Quarterly Perspectives are likely well versed in the goal-oriented nature of Appleton’s private client services. Wealth management is inherently personal, with each client’s objectives and risk tolerance shaping their investment plan. For this reason, we often recommend balanced strategies. While the equity exposure and underlying asset mix vary, the fundamental objective is to tailor asset allocation around individual financial objectives.

Including a high-quality bond allocation provides income that may be needed for retirement or to offset other future liabilities. It also provides a shock absorber that can help investors more comfortably withstand the inevitable volatility of riskier asset classes such as equities.

Experience tells us that emotional reactions to global events and market conditions are likely to be counterproductive. However, attempting to protect against these risks during a downturn can be too late. A more effective approach is to establish a diversified asset allocation strategy at the outset that addresses long-term objectives and reduces the likelihood of selling at the wrong time.

As we’ve long emphasized, sustained exposure to equities offers tremendous capital appreciation potential, yet this is best achieved through time in the market, not market timing. We believe that managing portfolio risk, in part through balanced portfolio construction, allows for greater comfort in staying invested, even when correlations occasionally turn positive.

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen, or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.