Insights and Observations

Economic, Public Policy, and Fed Developments

- Most of the world defines recessions as at least two consecutive quarters of GDP contraction. The US relies instead on an assessment by the National Bureau of Economic Research, which has not yet ruled. However, the release of the Q2 GDP advance estimate revealed a “technical recession” with a drop of -0.9%, slightly better than our expectations but well below the Bloomberg consensus estimate of +0.4%. Talk of recession has gained new urgency.

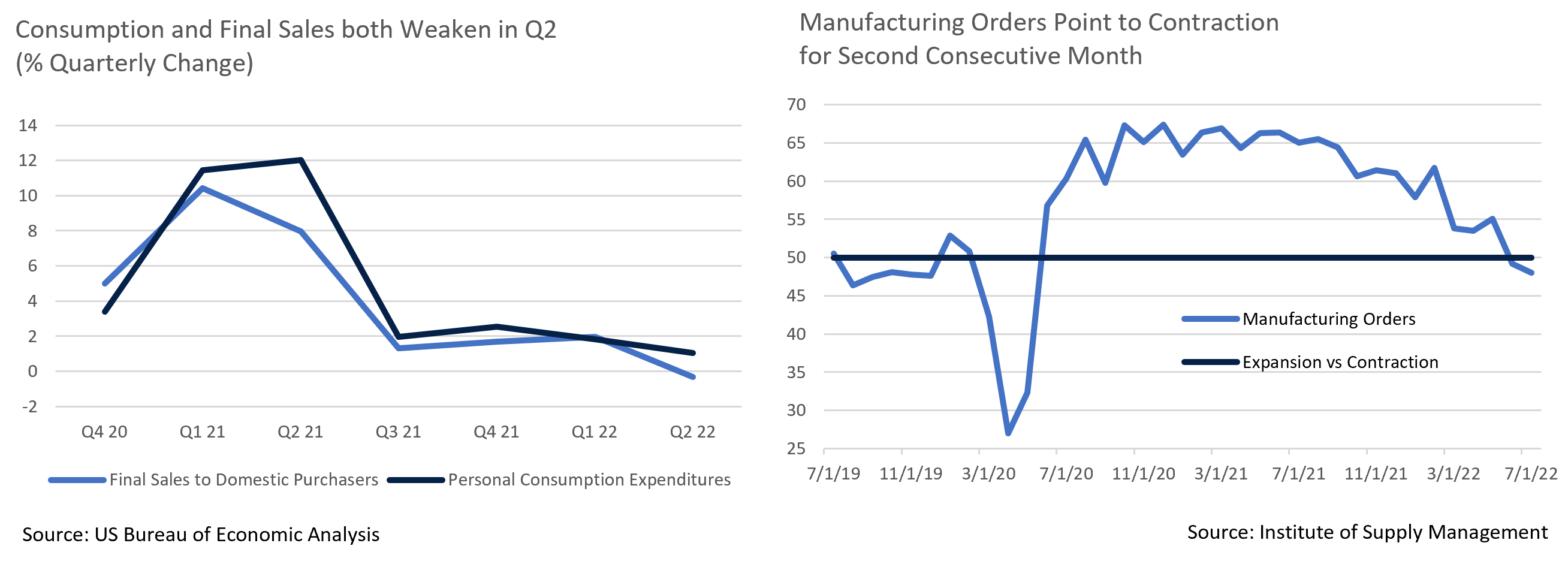

- While there is room to nitpick Q1’s contraction, the Q2 reading was unequivocally weak. A sharp drop in consumption and Final Sales to Domestic Purchasers falling from Q1’s +2.0% to -0.3% suggest broadening demand weakness. Other economic indicators also point to worsening conditions, most notably the ISM Manufacturing PMI now showing two consecutive contractions in their New Orders sub-index, and retail spending reports revealing spending falling in real terms. We believe the economy may already be in recession, but if not, it will be soon.

- The Biden Administration has pushed back on talk of recession, pointing to strong labor markets. And, while the June jobs report showed a stronger-than-expected 372k increase in unemployment, there is reason for concern. The accompanying household survey reported a contraction in employment of 315k jobs, closely in line with a 350k drop in the size of the workforce, which opens the door to a possible sizable downward revision in the June employment release. This would change the labor market narrative. Unemployment claims are still low but have ticked up steadily of late, and the number of job openings to unemployed workers is falling from elevated heights.

- In his press conference on July 28th, Chairman Powell made headlines for three related statements; the Fed would be dropping forward guidance and would become more data dependent, the future pace of interest rate hikes would likely slow, and the Fed had raised rates to a neutral level. We believe Powell’s remarks were misunderstood by the markets. Powell elaborated that the Fed’s last Summary of Economic Projections are still the best guide to their thinking, and they had communicated an anticipated slower pace in the fall for several months. Powell also described the neutral Fed Funds range as 2.25-2.50% based on a targeted inflation rate of 2%. Inflation is currently well above this level, indicating that the Fed’s current policy is still highly accommodative.

- The market took Powell’s comments as a suggestion the Fed would halt its interest rate increases sooner than expected, and rates – particularly shorter rates – fell sharply on the news. We think this interpretation is off base. The Fed has been transparent that inflation is its top priority and slowing demand to match a series of supply shocks is now a policy goal. The move in long term rates is more consistent with lowered expectations for economic growth over the next ten years, whereas the front of the curve, which is more closely tied to Fed Funds Rate policy, now appears mispriced. As a result, we expect the yield curve to invert further as market expectations adjust and shorter rates rise.

- Regardless of Fed policy, headline inflation should slow in August and September. A sizable drop in oil and gas prices occurred in June after the end of the CPI observation period and has continued through July. And while the impact may miss the July observation, a deal negotiated by Turkey and the EU allowed Ukraine to begin exporting grain from its port city of Odessa. Shortages had pushed global food prices higher and grain prices are now retreating. Core inflation very likely will prove stickier, and while a headline inflation decline would be welcome, we expect the Fed to remain focused on core. “

From the Trading Desk

Municipal Markets

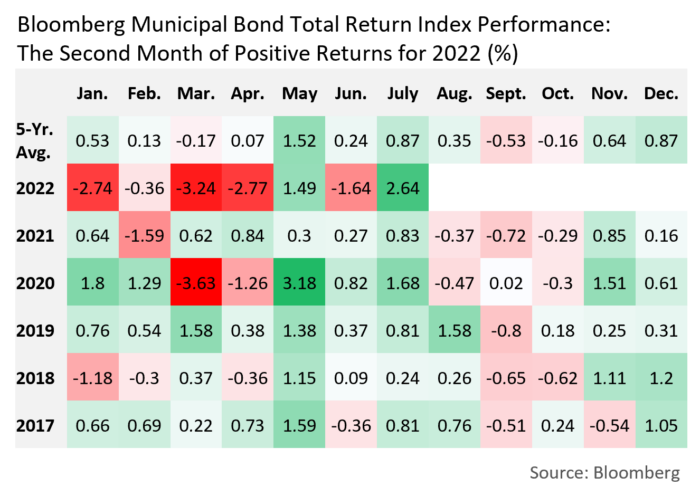

- Municipal bonds ended July with a positive month-end total return, performance that stood in stark contrast to losses posted at the end of June. July’s gains were driven largely by receding yield levels in the face of a slowing economy, seasonal cash roll creating more favorable technicals, and an uptick in retail flows. With $45 billion coming back into the market from maturities and reinvestment, we expect August to bring sustained demand.

- The week ended July 27th saw net fund inflows of $236 million reverse what had previously been 28 consecutive weeks of outflows according to Lipper Inc. The market’s tone has been stronger of late given lack of supply and a sense of urgency among buyers. Year-to-date issuance lags 2021 by 12%, and July issuance declined by 25% on a YoY basis with many deals oversubscribed. Less than $5 billion came to the new issue market over the last week. The bid side has been much stronger, leading municipals to outperform USTs.

- The month ended on a slow note as the market waited for the Fed meeting. Now that a 75 bps rate hike has been confirmed and Chairman Powell’s comments digested, traders are more assertively looking to move bonds and investors are seeking to get cash invested. This dynamic is making it challenging to find bonds at times but is supportive of bond prices.

- The front end of the municipal curve moved in tandem with longer maturities on Fed rate hikes, and unlike USTs, the curve remains solidly upwardly sloping. Spreads on the AAA curve between 2 and 10-year maturities stand at 61 bps, while the intermediate range between 5 and 10-years offers 41 bps of steepness. Longer maturity yield differentials widened considerably in July with 10 to 30-year spreads increasing from a relatively flat 25 bps to 69 bps.

Corporate Bond Markets

- In a reversal of the previous month’s direction, IG spreads retreated from a YTD OAS high of 160 bps to 144 bps. Risk assets rallied on increased recession fears and a slightly more dovish Fed tone. In addition, the surprisingly negative GDP number added to concerns about a slowing economy and weaker future growth prospects. Credit spread direction depends in part on how the Fed responds to economic conditions, although technical factors, which have been fairly stable, remain near term drivers. In our view, IG spreads should remain range bound and a breakout in either direction is unlikely.

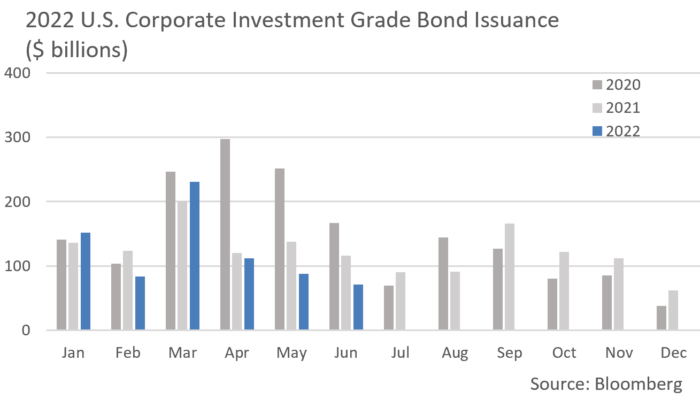

- A healthy return of issuance in July was well received by buyers. The month is typically a robust one in the primary market, particularly among financials, as issuers are fresh off earnings reports. Of the $90 billion in new debt brought to market, ~$58 billion came from financials. We have seen a shift in new issuance structure across sectors as issuers are favoring the front end of the curve. While shorter maturity UST rates are elevated, issuers appear to be weighing demand for shorter paper against higher concessions on longer term bonds. Lighter supply has been evident throughout 2022, as market volatility and uncertainty deters positive investor sentiment. Shorter maturity issuance should be the new norm for awhile, and we see stabilization of the primary market as a positive for credit spreads.

- High yield has been in favor as the risk asset rally was more pronounced than in IG. High yield spreads and yields dropped by the largest amount in nearly two years on the hope that the Fed will cool its rate hike momentum. In addition, better than expected earnings also contributed to the rally.

- A lack of issuance has been a contributor to spread action as only $1.835 billion hit the primary market last month, the slowest July in 16 years. Year-to-date issuance of $70 billion is the weakest since 2008. Although we do not buy high yield bonds, market conditions are an indicator of credit sentiment, and July’s high yield spread tightening may have been hasty given ongoing macro uncertainty.

Public Sector Watch

Credit Comments

ESG and the municipal markets

Environmental, social and governance (“ESG”) assessments long associated with equities and corporate bonds have also more recently become highly relevant tax-exempt research considerations. At Appleton, we believe that favorable ESG attributes are positively correlated with efficient municipal performance and, accordingly, developed a proprietary ESG scoring process that is applied to every tax-exempt bond issuer we evaluate.

Environmental, social and governance (“ESG”) assessments long associated with equities and corporate bonds have also more recently become highly relevant tax-exempt research considerations. At Appleton, we believe that favorable ESG attributes are positively correlated with efficient municipal performance and, accordingly, developed a proprietary ESG scoring process that is applied to every tax-exempt bond issuer we evaluate.

What are the primary benefits of municipal ESG analysis?

Our ESG scoring methodology allows our research team to evaluate and quantify bond issuer practices and risks, while offering a valuable input into fundamental credit research. ESG analysis gives us another tool to assess risks and relative value in the marketplace, while also facilitating an ability to customize ESG related SMA solutions for clients. Simply put, prioritizing these elements of credit research is additive to our investment decision-making.

What ESG factors do you consider when evaluating municipal bond issuers?

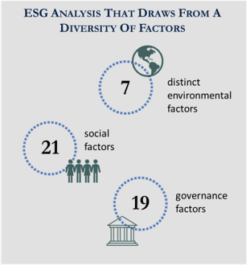

We evaluate up to 7 distinct environmental factors, 21 social factors, and 19 governance factors based on what is most relevant to the specific bond issuer. More specifically, social factors such as employment base, education, and poverty rates influence our view of the stability and growth potential of a local economy. Environmental factors such as fuel diversity and compliance with federal clean-water regulations reflect prudent management of electric and water utilities. Good governance is an important element of fiscal management and ultimately a municipality’s credit quality. Although we draw upon extensive quantitative inputs in bond issuer ESG analysis, there is also a qualitative element. This involves analyst assessment of factors such as management practices, natural risks, and litigation, among others.

How are Appleton’s municipal ESG scores calculated?

Each bond issuer is rated as “exceeding,” “good/adequate,” or “deficient” relative to sector medians in each factor chosen for evaluation. These factors are subsequently equally weighted and summed to arrive at issuer specific ESG scores of 1 to 5, with 1 being “deficient,” 2 to 3 “good/adequate,” and 4 to 5 representing “exceeding.”

What data supports your ability to analyze ESG criteria?

Our ESG research draws upon a wide range of valuable research sources. We utilize Investortools’ CreditScope as a research database as well as an analytical tool. Within CreditScope, we have access to a diversity of social and governance data for bond issuers to draw from in developing ESG characteristic analysis and/or in applying ESG related exclusions. We also access Moody’s ESG Solutions, a leader in analyzing, measuring, and projecting climate risk for cities and counties. Our research team incorporates their environmental data into our ESG model and scores the information based on Appleton’s proprietary formulas. Several other sources such as Bureau of Labor Statistics, and the FBI also offer important data inputs.

How do ESG scores relate to fundamental bond issuer credit ratings?

We begin all our tax-exempt credit analysis by evaluating traditional municipal credit metrics such as essentiality, economic base, and balance sheet strength. This leads to a preliminary issuer credit rating. Appleton’s ESG analysis is a separate process and Appleton assigned ESG scores are distinct from our proprietary credit ratings. However, a strong ESG score may be beneficial to the final credit research rating our analysts assign each bond issuer. Negative ESG evaluations often have the opposite influence and, in rare cases, may result in a “pass” rating on a bond issuer that precludes purchase.

There are potential limitations associated with allocating a portion of an investment portfolio in ESG securities. The number of these securities may be limited when compared to those that do not maintain such a mandate. ESG securities could underperform broad market indices. Investors must accept these limitations, including potential for underperformance. As with any type of investment (including any investment and/or investment strategies recommended and/or undertaken by Adviser), there can be no assurance that investment in ESG securities or funds will be profitable or prove successful.

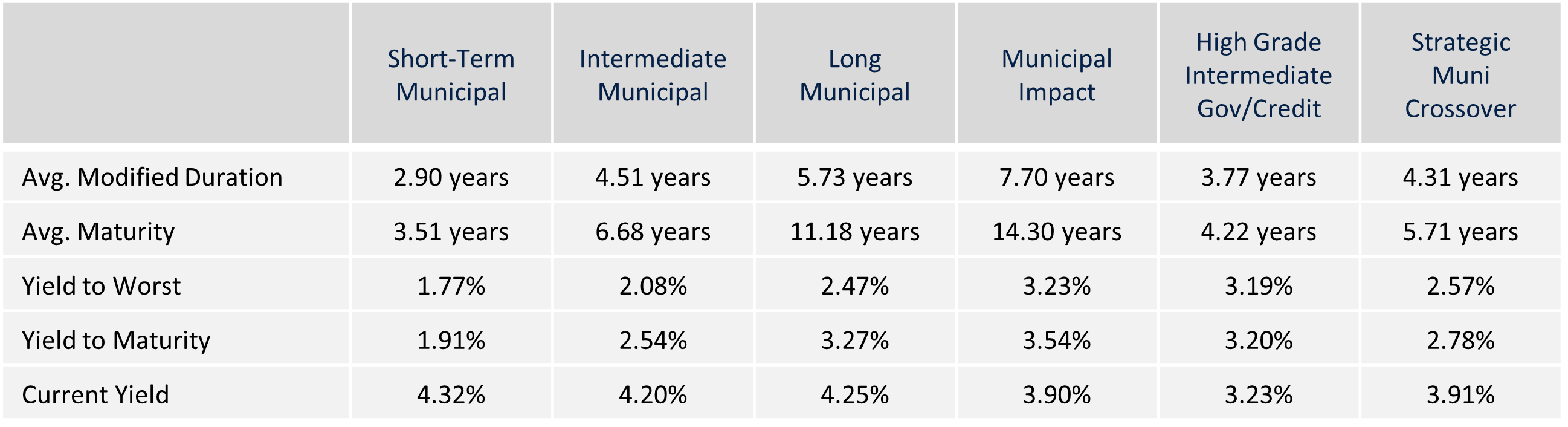

Composite Portfolio Positioning as of 7/31/2022

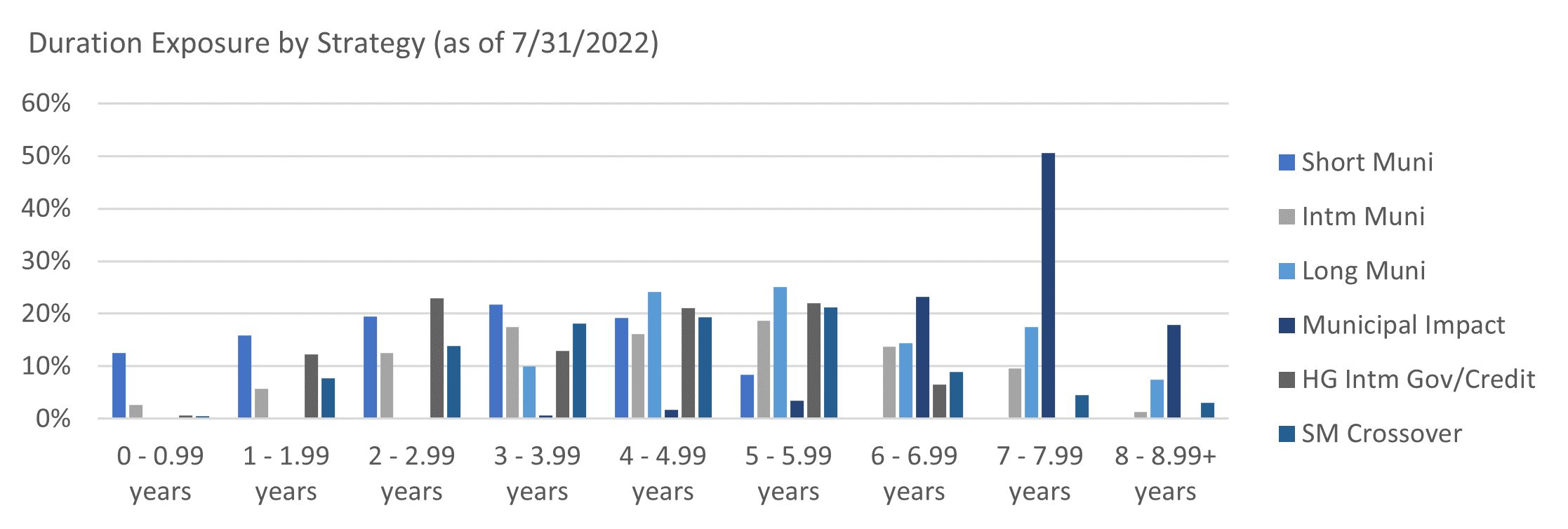

Duration Exposure as of 7/31/2022

Our Philosophy and Process

- Our objective is to preserve and grow your clients’ capital in a tax efficient manner.

- Dynamic active management and an emphasis on liquidity affords us the flexibility to react to changes in the credit, interest rate and yield curve environments.

- Dissecting the yield curve to target maturity exposure can help us capture value and capitalize on market inefficiencies as rate cycles change.

- Customized separate accounts are structured to meet your clients’ evolving tax, liquidity, risk tolerance and other unique needs.

- Intense credit research is applied within the liquid, high investment grade universe.

- Extensive fundamental, technical and economic analysis is utilized in making investment decisions.