Insights & Observations

Economic, Public Policy, and Fed Developments

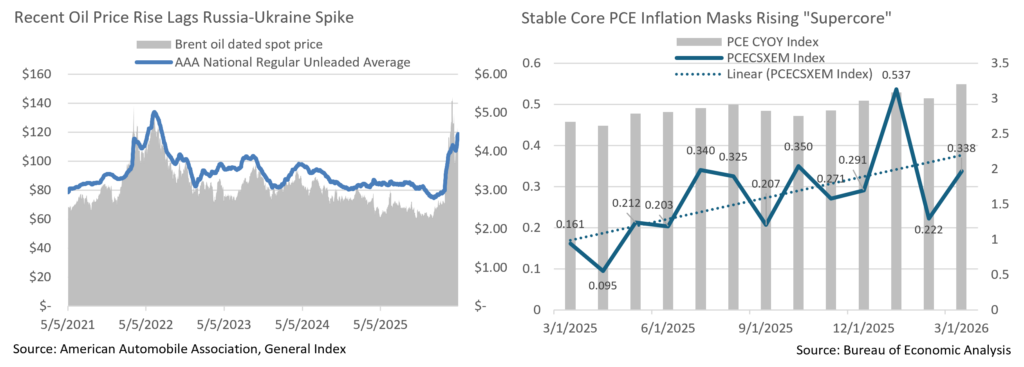

- April’s inflation data began to show the impact of the war in Iran, though so far it is narrowly contained. CPI was in-line at +0.9%, the highest reading since Covid, though encouragingly expectations fell as we got closer to the release, and core inflation came in a tenth lower at +0.2%. There is evidence of (very limited) consumer pullback in the most discretionary of categories; notable here in Boston at the start of baseball season was a 10% drop in admission to sporting events. This was one of a handful of large contractions to small components, without which we would likely have been in-line. So far, it appears consumers have not dramatically modified their behavior with surging gas prices, and energy costs haven’t yet begun to impact prices elsewhere.

- PCE, meanwhile was in line, at +0.7% headline and +0.3% core. However, we’re more focused on the Fed’s preferred “supercore,” which after a light reading in the prior month has reestablished an upwards trendline that’s largely been in place since Liberation Day. We remain concerned that core inflation was moving against the Fed even prior to the war.

- Retail spending surprised strongly to the upside, +1.7% vs +1.4%. While these are nominal and not inflation-adjusted measures, and accordingly the headline was boosted by higher gas prices, the “control group” (which strips out a number of components, including gas) rising 0.7% vs 0.2% suggests real strength. This comes at a time when many consumers received fairly robust tax refunds, so it will be interesting to see if this strength continues.

- After March’s jump, gas prices were largely stable for most of April but surged in the final week of the month. Price moves have so far lagged what we saw after the 2022 invasion of Ukraine; however, we see room for gas prices to potentially rise further from here. The Trump Administration has responded by tapping the Strategic Oil Reserve (as did the Biden Administration post-Ukraine) and at the current pace will be able to draw down through October before reaching the legal minimum and approaching levels where the stability of the underground network might become at risk. High gas prices are likely to linger beyond then even in the event of a rapid resolution of the war, which we do not see. We would note that despite both parties’ rhetoric to the contrary, the US has been de-escalating when given opportunities to escalate, while Iran has been escalating when given opportunities to de-escalate. This suggests peace is not yet likely.

- Powell’s final meeting as chair of the FOMC was full of surprises, despite widespread consensus that rates would be held unchanged. Powell’s decision to stay on the Board of Governors through the end of his term in 2028 after he leaves as Chair at the end of this month cited legal attacks on the Fed’s independence (by convention the Chair usually resigns) and was not unexpected. We believe that one consequence of this decision has been underappreciated; as incoming Chair, Kevin Warsh, will now replace uber-dove Steven Miran rather than Powell, making Warsh a net hawkishaddition to the FOMC.

- This is important in the context of the meeting’s biggest surprise; there were four dissents, the most since 1992. Miran’s dissent in favor of a cut was assumed, but Kashkari, Hammack, and Logan dissenting due to a perceived “easing bias” in the Fed statement (notable in that the actual statement was remarkably neutral) was completely unexpected. We believe this was a shot across the bow, less to Warsh than to the Trump Administration, implying that no matter who chairs the FOMC, the votes to cut interest rates don’t exist. With the Iran War pressuring oil markets and inflation, the market is at least well aligned with this view, and at present no rate adjustments are priced in through 2027, supporting our view that the Fed is on hold until they have a clear reason not to be.

Sources: Bureau of Labor Statistics, Bureau of Economic Analysis, U.S. Census Bureau

Equity News and Notes

A Look At The Markets

- Stocks were meaningfully higher in April as the S&P 500 gained +10.4%, its best month since November 2020. The index erased all war-related losses by the middle of the month and ended April at an all-time high while riding a 5-week winning streak. The tech-heavy Nasdaq outperformed, also closing the month at an all-time high while gaining +15.3%, its best month since April 2020. The DJIA, which tends to lag during risk-on periods, underperformed with a +7.1% gain and still sits below its February all-time high. Traders piled back into growthier pockets of the market with Communication Servies (+18.4%), Technology (+17.4%), and Consumer Discretion (+11.7%) the only three sectors to outpace the overall market. Only two sectors closed lower, with traders largely shunning defensive Health Care (-0.6%), and Energy (-3.5%), both of which gave back some of its prior month’s gains.

- With a fragile ceasefire in place, traders have tried to look past the conflict in Iran despite WTI crude ending the month at $105 per barrel. The potential remains for higher oil prices, higher inflation expectations, and subsequent higher interest rates to weigh on risk sentiment, but that is all being outweighed by the AI boom…for now. Mega-cap tech outperformed in April, with the “Mag 7” gaining +14.9%, but the real move was in semiconductors, as measured by the SOX. The SOX rose +38.4%, enjoying an 18-day win streak, its longest ever, to bring its past 12-month gain to an eye-popping +148%. Counter to the trend over the first quarter, breadth tightened on Tech’s strength as the equal-weight S&P 500 (RSP) trailed the market-cap weighted index by 4.4%. Narrow leadership is nothing new for this bull market, and the RSP still remains ~0.9% ahead YTD, but we would prefer to see more participation and a broadening out of the AI trade.

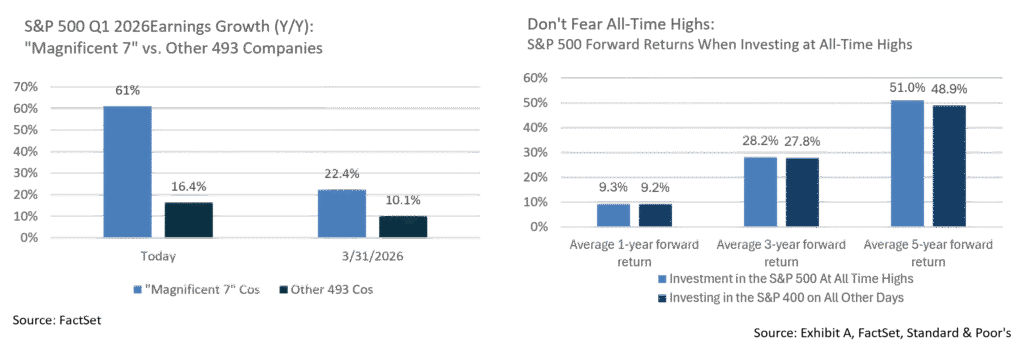

- Corporate profits and the ongoing Q1 earnings season represented a principal reason why the market was able to hit highs amid the fog of war. With nearly 67% of S&P 500 companies having reported by month-end, the earnings beat rate (84%) and beat margin (+20.7%) are both well ahead of historical averages. With more companies beating and doing so by a wider margin, the blended earnings growth rate has improved to +27.1%, which would mark the highest YoY growth rate since Q4 2021. For context, expectations were for +13.1% coming into the quarter. Net profit margins are also well above average at 14.7%, the highest level since at least 2009.

- There are, however, reasons to temper enthusiasm. First, the earnings growth is largely driven by the “Mag 7,” a group growing at +61% YoY. The other 493 companies are growing at a very respectable +22.4%, but the gap is widening which could lead to further breadth narrowing. Second, is the number of one-time items being included in the GAAP earnings figures. Two examples are a $37.7 billion gain for Alphabet on unmarketable equity securities, and a $16.8 billion gain reported by Amazon on pre-tax gain in their Anthropic investment. The inclusion of one-time items is common practice, but they are not part of the daily operations of these companies, therefore, nuance is required when evaluating results.

- A popular adage advises one to “sell in May and go away” and is based on historical returns that show that returns from May through October tend to lag November through April. While true, it’s important to remember that the period from May through October has still averaged a +6.9% return over the past 10 years. The trend heading into the period is often the determining factor. Looking at the past 25 occurrences when the S&P 500 was up >+5% through April, the average return for the remainder of the year was +8.8%, and it has been positive 23 out of 25 times. Another hang-up for investors is investing at all-time highs, fearing a market timing mistake. Putting money to work at all-time highs, particularly with a long-term focus, has historically resulted in slightly better returns. Going back to market sayings, one we firmly believe in is that “time in the market beats timing the market.”

Sources: Bloomberg, FactSet

From the Trading Desk

Municipal Markets

- After seeing both rates and ratios rise sharply during March, investors opportunistically took advantage of an attractive yield landscape and appealing ratios in April, a month that appears to have been a good entry point during a seasonally weak period. As such, price action reversed course but not enough to fully offset the prior month’s backup.

- Apart from 1- and 2-yr maturities, municipal rates rallied top to bottom, from a few basis points in the front-end to as much as 20bps in the belly of the curve.

- With regards to absolute yield moves, the 1-yr maturity saw yields push higher by 16bps. while the 2-yr saw a more tapered selloff of 5bps. Maturities in 3-, 5- and 7-yr spots rallied by 2, 8, and 11bps, respectively, while the 10-yr and longer part of the curve registered lower yields of 16-20bps.

- The rally pushed AAA Muni/Treasury ratios lower for all spots on the curve other than the front end which saw sustained relative cheapening. The 3- and 5-yr maturities richened by 1.7-3%, while 7 to 30-yr ratios tightened by 3.75%-4.65%, the most notable move being in the 10-yr spot. The month closed with the 3-yr ratio at 63.5%, 5-yr at 64.7%, while the 10-yr settled at 68%. At the long end of the range, the 25- and 30-yr spots closed at approximately 80% and 87%, respectively.

- According to JP Morgan, April produced tax-exempt issuance of $43B, more than 25% above the trailing 5-year average ($34B) and tying last April as the second-highest issuance April on record.

- Municipal funds continued to see robust subscription activity throughout the month with April’s fund flow estimate totaling about $3 billion according to Barclays. The primary asset gathering categories have been ETFs and long-term/national funds.

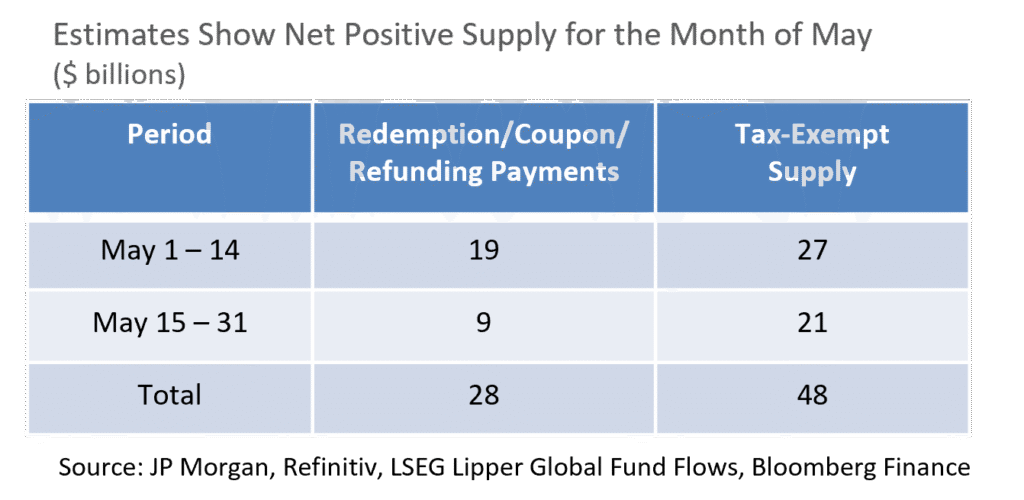

- Sustained fund inflows have helped absorb increased issuance and resulted in the asset class posting a healthy total return of +1.15% in April, the best since 2014 according to JPMorgan. May looks to be somewhat more challenging from a technicals perspective with net positive supply estimated at around $20B, the equivalent of the prior 4 months of net supply combined into a single month, according to JPMorgan. As such, attractive opportunities to add to municipal exposure may emerge.

Corporate Markets

- US Treasury rates climbed higher with a curve steepener firmly in place. The largest move across the curve was the 8bp increase in the 2-3-Yr maturities. In addition, when measuring the move so far this year, the 2-Yr portion the curve has moved higher by 40bps. Second to that was the 3-Yr at 35bps, while the 10-Yr moved higher by just 20bps in that time. The curve inversion on the short end has been erased, for now. The trajectory of short-term rates will continue to be driven by the market’s reaction to the Fed, and while the recent Chairman change shouldn’t change policy immediately, we do feel that volatility will remain.

- US Investment Grade credit spreads dropped 10bps during April, with the 79bps OAS month end print on the Bloomberg US Corporate Bond Index the lowest level since the end of February of this year. It’s also 14bps off the YTD high in mid-March. While there is concern given what’s happening in the Middle East, risk sentiment continues to be in the “on” direction with investor demand being very high. Elevated rate levels and a stable credit environment is offering opportunities for investors with an appetite for yield. The direction in spreads continues to feel very narrow and a breakout does not appear to be likely.

- We saw a minimal amount of movement in spreads within individual rating buckets over the course of April. The largest spread move occurred within the BBB vs AA category where the spread narrowed by 6bps to a difference of just 40bps. This encapsulates a large portion of the market and the spread between BBB and A tightened by just 3bps. April saw lower quality performing better than higher rated bonds. Our preference for higher quality bonds remains intact especially as spread compression in lower quality diminishes the risk/reward component of the lower rung of the quality spectrum.

- Issuers continue to take advantage of investor demand that has had a significant appetite for bonds. The month’s $177.52B brought to market beat the $115B syndicate estimates for April. Several jumbo deals helped to push levels higher, bringing the YTD total to $813.55B, 26% higher than this time last year. Buyer fatigue generally feels nonexistent, with many deals receiving orders that amounted to nearly 4 – 5 times more than available bonds. It is expected that May will be another big month for issuance with estimates well over $100B. It may be the last big push before summer sets in but there is no sign of issuers letting up anytime soon.

Sources: Bloomberg, Bond Buyer, Barclays, JP Morgan, and Lipper Inc.

Financial Planning Perspectives

Wealth Tax Proposals Prompt Tax Planning Considerations

Several states have recently introduced or proposed new taxes aimed at wealthy households. At the end of March, the State of Washington passed a Millionaires Tax, which will impose a 9.9% tax on households earning over $1 million annually beginning in 2028. Virginia lawmakers are now considering a Wealth Proceeds Tax that would apply a 10% tax to households earning more than $1 million per year. California has also proposed a one-time 5% tax on residents with assets exceeding $1 billion, excluding directly held real estate. Most of these proposals refer to the Massachusetts’ Millionaires Tax which was enacted in 2022 and added a 4% surtax on adjusted household income over $1 million, a figure that adjusts annually for inflation. Revenue generated from the tax has so far exceeded expectations.

Taxes of this nature have generated considerable debate in an already charged political environment. Supporters argue that these measures are needed to help address rapidly growing wealth inequality while generating additional revenue to fund services and reduce budget deficits. Opponents consider the taxes punitive and raise concerns that the complexity and cost of implementation erode potential benefits.

For example, state tax authorities would need to begin auditing non-financial assets such as homes and collectibles. In addition, critics also question whether projected revenue will ultimately meet expectations, as many impacted individuals will likely engage in tax planning strategies, restructure assets, or consider relocating to lower-tax jurisdictions.

Clients who could be impacted by newly introduced or proposed taxes may want to consider several planning approaches. Evaluating whether certain assets could be transferred to an irrevocable trust is a potential option, with the appropriate structure dependent on the client’s specific circumstances and objectives. For clients who are already charitably inclined, or those interested in incorporating philanthropy into their financial plan but unsure where to begin, developing a formal giving strategy and exploring vehicles such as donor-advised funds or charitable trusts may be beneficial. For those already contemplating a move for family or lifestyle reasons, conducting a tax impact analysis across different states can help further inform the decision.

At a minimum, revisiting your financial plan to assess the potential effects of newly introduced or proposed taxes is a prudent step. Your Wealth Management team is available to help evaluate considerations of this nature and to discuss complex financial and tax planning issues relevant to your situation.

Congratulations to Appleton’s Jennifer M. Hall, CFP®, AEP®, on being elected to the Boston Estate Planning Council’s board of At-Large Directors. The Board of Directors at BEPC oversees operations and sets strategic direction for the organization. At Appleton, Jen serves as a Wealth Manager, a role in which she collaborates with attorneys, accountants, and trustees to help individuals, families, and nonprofit organizations achieve their financial planning and wealth management goals. She is an active member of BEPC, currently serves as a committee chair, and is a past recipient of the BEPC President’s Award, recognized for her leadership and commitment to the Council’s community engagement and financial literacy initiatives.

Sources: https://www.pgpf.org/article/what-is-a-wealth-tax-and-should-the-united-states-have-one/, https://www.cnbc.com/2026/04/23/wealth-tax-millionaire-tax.html, https://www.barrons.com/articles/wealth-taxes-saving-for-rich-11d6cd06, Appleton Partners, Inc.

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen, or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.