Insights & Observations

Economic, Public Policy, and Fed Developments

- For some time now our view has been that the labor markets are somewhat stronger and progress lowering inflation is somewhat weaker than the market consensus holds. Nothing has fundamentally changed this view, but quite a lot happened in February that we think deserves attention.

- As expected, in a 6-3 decision, the Supreme Court found the Trump Administration’s use of the International Emergency Economic Policies Act to apply tariffs without Congressional review unconstitutional (notably, the dissents were focused more on disruption than legal questions). Trump wasted little time turning to a new avenue, applying tariffs under Section 122, a legally vetted mechanism that allows him to do so up to 15% for up to 150 days without Congressional action. We believe exact rates are less important than the point at which companies can consider tariffs “settled” and begin to plan around them; this adds significant uncertainty.

- In the short term, with rebates possible but ongoing tariff levels only slightly lower, there was not much movement in longer rates. We are monitoring discussion around rebates, which are likely, though the possibility of Congress authorizing payments to American citizens (without also a directive to not rebate importing companies) remains a risk, as this would double the budgetary impact of the Court decision and could impact longer rates.

- January’s Nonfarm Payrolls report had little notto like; employment growth doubled expectations, at 130k, the unemployment rate fell a tenth and nearly rounded to a two tenths improvement, in the Household survey both participation and employment rose substantially, sustaining strong growth since mid-summer, and earnings growth was respectable. Expectations for February remain low, with a Bloomberg consensus of 59k and an unchanged unemployment rate of 4.3%. All the same, a market consensus that the Fed needs to lower rates to support the labor market is hard to square with what looks like healthy labor conditions.

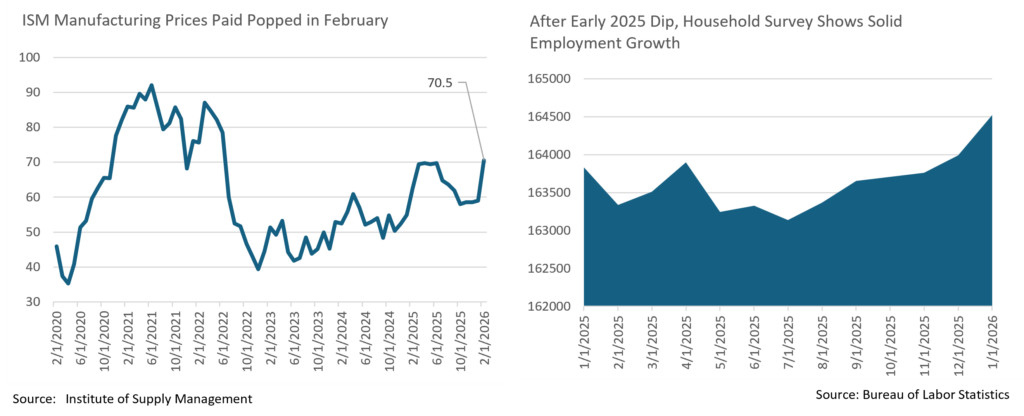

- Markets positively reacted to the January CPI report, despite our misgivings (our February white paper discussed this issue). Subsequent data has done a good job demonstrating why we are concerned. The first Fed Beige Book of the year showed companies that hadn’t yet passed along tariffs were starting to capitulate and raise prices. For nearly a year now we’ve been concerned that uncertainty around tariff policy was stretching this pass-thru process out. A hot PPI report with a large contribution from trade services (implying margin expansion, we believe from compressed levels where tariffs were being absorbed), and an unexpected surge in the Prices Paid component of the ISM Manufacturing index to the highest level since 2022 gave credence to this survey. We continue to expect a reacceleration of inflation in the first half of 2026.

- Joint US and Israeli strikes on Iran were the final unexpected macro development bookending February. The initial rate move was down, to nearly 3.92% on the 10Yr at the lows, but interestingly as it became clearer that this conflict could last at least several weeks, rates reversed. As of morningtrading on Tuesday, March 3rd,the 10Yr was back over 4.10%. Some of this move is a market reaction to the ISM Prices data, but we also suspect that the traditional “flight to quality” may have been overpowered by a combination of concerns over the war’s impact on inflation, and the potential for larger US deficits if military action is prolonged.

Sources: Bloomberg, Bureau of Labor Statistics, Institute of Supply Management, the Federal Reserve

Equity News and Notes

A Look At The Markets

- Stocks were mixed in February with the S&P 500 dropping -0.9% to cut its YTD total return to +0.7%, and the Nasdaq (-3.4%) logging its worst month since March 2025. The Russell 2000 (+0.7%) and DJIA (+0.2%) both outperformed with the Dow extending its monthly win streak to ten. Despite the headline weakness, only four sectors were down on the month with Consumer Discretionary (-5.4%) and Communication Services (-5.1%) the hardest hit. A mix of cyclical and defensive sectors surged with Utilities (+9.9%), Energy (+8.8%), Materials (+8.3%), and Consumer Staples (+7.9%) all meaningfully outperforming.

- AI disruption was a key theme as optimism morphed into fears that AI models would become increasingly capable of replacing white-collar jobs. Traders adopted a “shoot first, ask questions later” mentality and aggressively sold stocks in numerous industries, most notably software, but also wealth managers, insurance brokers, real estate services, and even trucking and logistics. The “AI scare” trade gained steam at the end of the month when a little-known research firm, Citrini, released a thought experiment painting a bearish, dystopian view of the economy in 2028.

- Fears were not contained to the public equity markets as private credit concerns popped up and multiple funds were feared to be halting redemptions or cutting dividends given their large concentration of loans to tech companies. At this point, we believe that trading in some of these pockets of the market is not based on fundamentals and that the “baby is getting thrown out with the bathwater.” The impact of AI is real, but will be uneven, gradual, and difficult to predict, so we remain diligent in looking for opportunities.

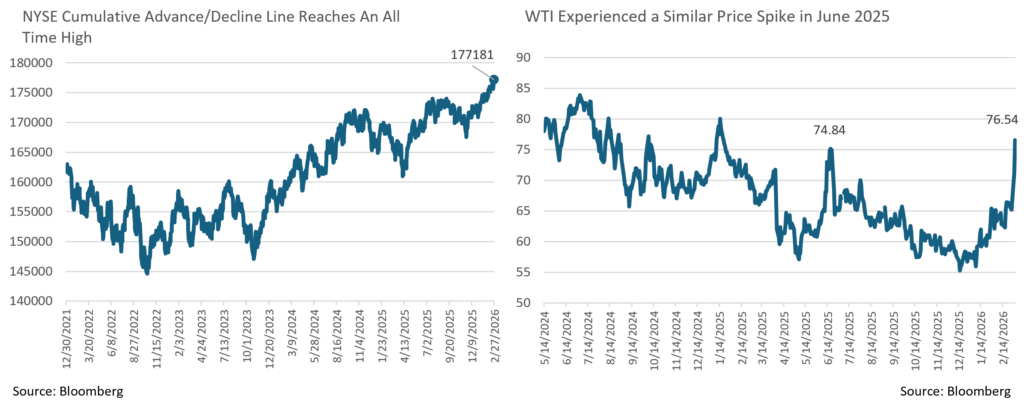

- Despite AI concerns, the S&P 500 has been remarkably calm on the surface with a 2.7% trading range for YTD closing prices the smallest range in history. Below the surface has been anything but serene though as the index has more companies trading +/- 20% YTD (122) than +/- 5% (119). With technology shares under pressure, investors have taken profits in the “Mag 7” (-6.8% YTD) and rotated into so-called “HALO” (heavy asset, low obsolescence) stocks in industries such as food, beverages and tobacco, energy, retailers, and telecom. This shift has led to notable outperformance from the equal-weight S&P 500, which is now +7.0% YTD and at an all-time high. We view this breadth thrust as favorable, and market internals are confirming as the NYSE cumulative A/D line is at an all-time high and over two-thirds of the S&P 500 is above its respective 200-day moving average.

- Markets do not stay rangebound forever and fresh geopolitical tensions in the Middle East are currently roiling markets. Uncertainty abounds as joint strikes against Iran by the US and Israel over the weekend have traders on edge. Like June 2025 when the US struck Iran, WTI crude oil has spiked above $70/barrel on fears of supply disruptions. In turn, bond yields are beginning to move higher after an initial flight to quality as traders fret about oil’s impact on inflation and whether the Fed will deliver as many rate cuts as expected this year. As we discussed last month, geopolitical flare-ups have historically proven to be buying opportunities, and it will be interesting to see the extent of the Administration’s tolerance for stock and bond market pain as the midterm election season heats up. It is also worth watching to see if the US market will outperform much of the rest of the world given the extent to which our economy has become less dependent on foreign oil over recent decades.

Sources: Bloomberg, FactSet

From the Trading Desk

Municipal Markets

- Municipal performance remained strong in February, buoyed by significant intra-month redemptions (est. at >$40B) and fund subscriptions.

- Municipal yields rallied in a largely parallel fashion with the most significant move in the 15-year spot on the curve. The 2s-30s curve went net steeper by 3bps but effectively twisted. The slope inside of 10 years steepened by 1-3bps, while 10s-15s flattened by 8bps as more market participants pushed out the curve in search of value.

- With regards to absolute yield moves, 5-year issues and shorter fell by anywhere from 14-to-16bps. The 7- to-12-year maturities moved lower in a similar fashion, notably by 11-13bps, while the 15-year spot experienced the most aggressive move down in yield, declining by 19bps. The long end (25- to-30-years) finished the month lower by 16bps and 12bps, respectively.

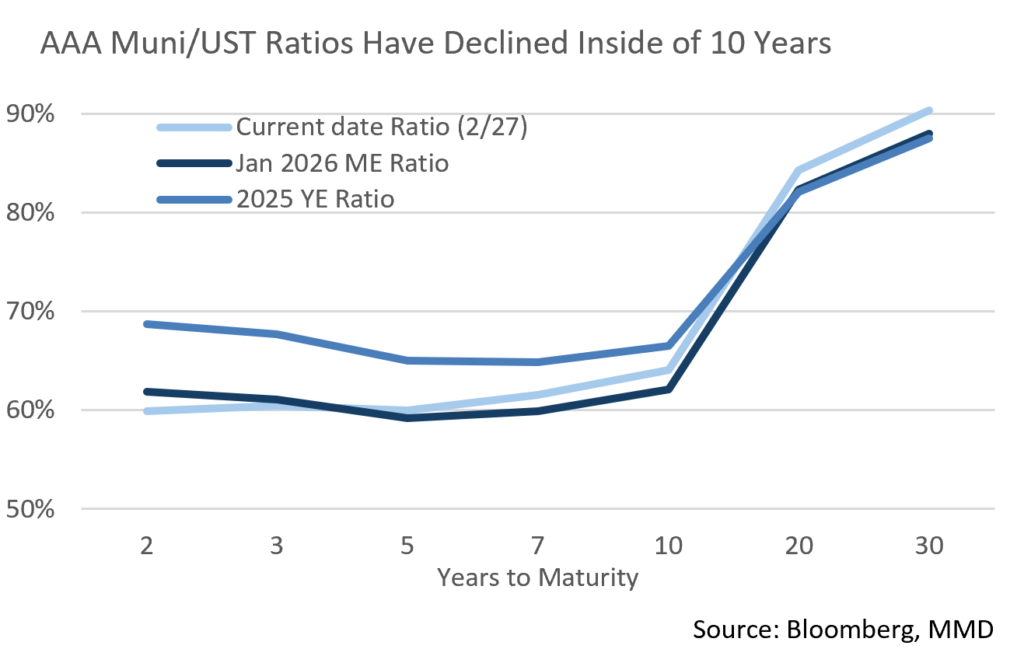

- Municipal ratio moves were more muted after the significant strength of the prior month. Ratios in the 2- and 3-year range moved slightly tighter by 2% and 0.66%, respectively, while all maturity points of 5-years and longer saw slightly cheaper ratios, within a range of 0.79-2.32%. The month closed with the 3-year ratio at 60.4%, 5-year at 59.9%, and the 10-year settled at 64%. On the long end, the 30-year maturity widened to 90.3%.

- According to JP Morgan, February tax-exempt issuance totaled $40B. From a relative standpoint, long-term tax-exempt supply set a new high-water mark in February, besting the prior records of $37B in 2007 and $36B for 2025.

- Market technicals should weaken in March in line with seasonal expectations, with redemption capital estimated at $32B vs. estimated supply of $41B. This could loosen up tight ratios and unlock opportunities for tax-exempt investors.

Corporate Markets

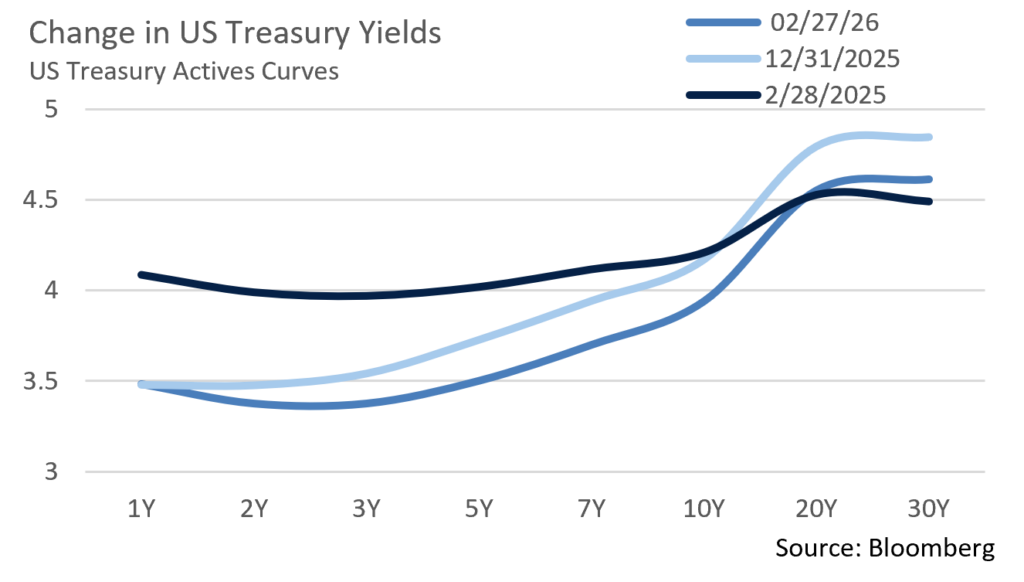

- Treasury yields fell significantly in February, largely driven by a month-end rally into safe havens. The curve shifted down in a parallel manner that retained prevailing steepness over 2 to 20-year maturities. However, this move deepened a yield trough between very short issues through the 7-year part of the curve. For example, the 7-year benchmark dropped 31bps to 3.71%, a level that was only 3bps higher than the 4-month T-Bill which did not move in yield. Benchmark 10-year, 20-year, and 30-year bonds all moved lower by 26 to 29bps with the 10-year closing at 3.95%.

- The economic picture, particularly inflation pressures exacerbated by the US and Israeli attacks on Iran, may keep the Federal Reserve on hold for the time being. Rising global tensions could produce a further “risk-off” move towards assets such as Treasuries, placing downward pressure on yields.

- After tightening to begin the year, US Investment Grade credit spreads retreated in February. A 73bps OAS spread on the Bloomberg US IG Corporate Index rose to 84 bps by month’s end, the highest level so far in 2026. While the Index produced positive returns, the effects of widening created negative excess returns vs. Treasuries. Global market uncertainly is to blame here, not credit concerns. Demand for IG credit remains strong, and we feel that modest widening of credit spreads is healthy given the relative tightness the market has long been experiencing. Over the near term, additional widening is likely although we expect investor demand to dampen the magnitude of this move.

- The Investment Grade primary market remains robust and the landscape for issuers is still attractive. Concession levels are still very low and almost non-existent for high quality deals. The $190.9B of new debt issued MTD is right on the target set by the syndicate. That included a $20B jumbo deal brought late in the month and a similar-sized deal in January. Expectations for the March calendar are high at $230B although war in the Middle East has already left issues on the sidelines while more offerings may be delayed in the weeks to come. At this point, YTD expectations for $1.85T remain in place.

Sources: Bloomberg, Bond Buyer, Barclays, JP Morgan, and Lipper Inc.

Financial Planning Perspectives

The Power of Simplicity: Why Account Consolidation Matters

In today’s financial world, it is common to accumulate accounts over time. Whether it is a 401(k) from a previous employer, an old IRA, a brokerage account opened years ago, a college savings plan, or perhaps even an account managed by a prior advisor. Individually, each account may serve a purpose, although collectively, maintaining certain legacy accounts can create unnecessary complexity.

Account consolidation is a planning strategy that is often overlooked, but one that can be impactful as it offers an opportunity to meaningfully improve financial planning analysis, efficiency, and long-term results.

Transparency Creates Clarity and Better Oversight

When assets are spread across multiple custodians and platforms, it becomes difficult to identify and manage overall asset allocation. You may believe you are diversified or otherwise invested in a given manner, yet without a consolidated view of your assets, risk concentrations, duplicated exposures, or other unintended risks may go unnoticed. Consolidating accounts allows us to:

- View your asset allocation on a more holistic basis

- Ensure investments are aligned with your long-term plan

- Eliminate redundancy or unnecessary overlap

- More effectively engage in disciplined rebalancing

Improved Tax Awareness and Planning

Tax efficiency is not just about what you earn, it is about what you keep. When accounts are consolidated, we are better able to help you benefit from:

- Opportunities for tax loss harvesting

- Managing embedded capital gains in various taxable accounts

- Seeking to place investments based on their tax status and efficiency

- Efficient retirement income withdrawal strategies

- Consolidation allows us to be proactive rather than reactive.

Streamlined Reporting and Organization

A greater number of accounts will typically introduce additional statements, logins, and tax forms. At tax time, this can translate into more administrative work and an increased risk of errors or missed tax management opportunities.

Streamlining accounts is a planning step that often has considerable benefits, including:

- Simplified performance reporting

- Coordinated beneficiary designations

- Reduced paperwork for you and your CPA

Financial organization not only adds convenience, but it can also improve decision-making.

Effective Risk Management

When portfolios are spread across several different accounts one’s view of risk can be distorted. For example, one account may be conservatively positioned while another is aggressive. Individually, that may seem reasonable, but collectively your overall risk profile may not be optimally aligned.

Estate Planning and Legacy Clarity

Maintaining too many accounts can also create issues for future beneficiaries and complicate eventual asset transition. Consolidating portfolios into fewer accounts can help to:

- Ensure titling is clear and beneficiaries are aligned

- Transfer processes are efficient

- Reduce administrative hurdles during emotionally difficult times

Reorganizing today can produce a smoother process for your family tomorrow.

Sources: https://www.troweprice.com/personal-investing/resources/insights/should-you-streamline-your-retirement-savings.html; https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/taxes/coordinated-approach-to-multi-account-management.pdf

Financial Planning Perspectives Sub-header H3This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen, or experience. Investments in securities are