Insights and Observations

Economic, Public Policy, and Fed Developments

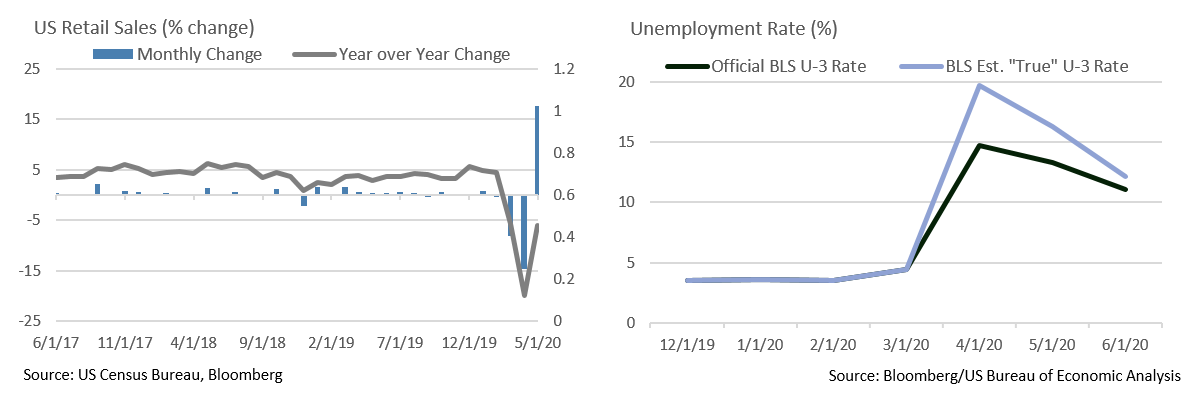

- As COVID-19 continues to roil the labor markets, it has presented several challenges to interpreting jobs reports. One of the biggest is related to a mistake the Bureau of Labor Statistics (BLS) acknowledged in their release – a large number of workers who were temporarily laid off due to the pandemic were misclassified as “employed but absent from work” in surveys, causing the unemployment rate to be understated. They estimate this impacted 5 million workers in April. BLS reported unadjusted survey data but estimated that the April and May rates should have been 5 and 3 percent higher, with June much improved but still one point higher than reported.

- The second issue concerns how likely these gains are to be sustained. June’s Employment Situation report showed the unemployment rate dropping from 13.3% to 11.1% as the economy added 4.8 million new jobs. However, the bulk of these jobs – 2.1 million – were in service industries, and with parts of the country experiencing a surge in COVID-19 cases, some of these job gains may not last. Given the pace of COVID-related developments, jobs reports are likely a lagging indicator, and while we welcome the improvement in employment, we are not yet confident in its durability.

- The labor market also faces stubbornly high initial unemployment claims. After a sharp drop in May, weekly initial claims have leveled off, most recently to 1.4 million, little changed from the beginning of June. Continuing claims remain around 19.3 million. Some of the elevated levels after the initial spike were likely related to delays in an overwhelmed unemployment system, yet the longer claim levels remain elevated the less compelling that explanation becomes.

- Personal income fell 4.2% in May, a smaller than expected drop given the slowdown in government aid (which will continue to fall unless stimulus programs are renewed). Spending increased 8.1%, substantial but not nearly enough to offset March and April’s weakness. Personal savings fell, though to a still exceptional 23.2%. Customers seem to be proceeding carefully with their finances in the absence of clarity regarding how and when this pandemic will end.

- This was evident in May retail sales, which were unexpectedly strong, rising by 17.7%, nearly three times the Bloomberg median expectation of 5.6%, after an upwardly revised drop of 14.7% in April. Interviews conducted by the WSJ suggest American consumers are redirecting rather than increasing spending; money originally earmarked for vacations or to be spent on services is instead going towards “at home” items, while also paying down debt and/or increasing savings. Total retail sales are down 6.1% YoY.

- The Federal Reserve signaled in clear terms during their meeting of June 9 and 10 that ultra-low rates are here to stay. The Fed “dot plot” of rate expectations showed the Fed Funds rate remaining on hold through at least 2022, and in his testimony, Jerome Powell quipped that it was difficult to even think about thinking about raising rates. The Fed also indicated that the current pace of bond-buying would continue over the near term, which most market participants interpreted as into September.

- While still on the backburner relative to the pandemic, trade tensions once again flared in June. The US refused to certify Hong Kong’s independence at the start of the month in response to a national security bill proposed by China. The actual bill enacted on July 1 ended up being far stronger and more vaguely worded than expected, prompting protests. Meanwhile, President Trump authorized $3.1 billion in new tariffs on EU goods, corresponding with the six-month review of tariffs in retaliation for Brussels’ illegal Airbus subsidies. The EU is working on $11.2 billion in new tariffs of their own pending the WTO’s decision on US subsidies for Boeing due in September. Renewed trade hostilities could not come at a worse time given the fragile state of the global economy.

Equity News and Notes

A Look at the Markets

- The S&P 500 jumped 20.5% during Q2, the largest quarterly advance in over 20 years. The Index remarkably recouped nearly all of its earlier 2020 losses, closing the first half down only 3%. The gains were largely driven by historic fiscal and monetary policy support, along with data that showed that the economy was beginning to recover.

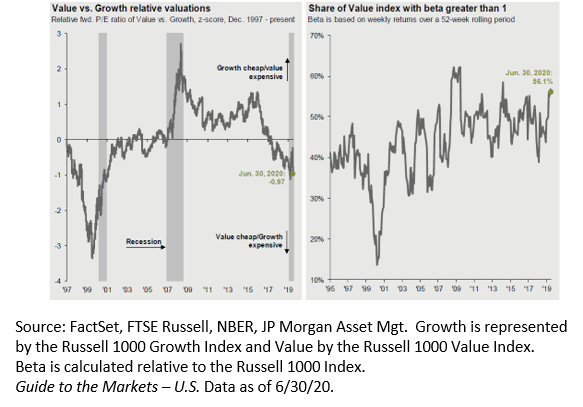

- Some things remain unchanged, with growth stocks continuing to outpace their value counterparts, especially among large cap names. The growth style is largely made up of Technology and Healthcare stocks, sectors that are likely to see continued spending over the remainder of 2020. The tech-heavy Nasdaq closed the quarter near all-time highs after posting a YTD gain of 12.5%. A trend worth noting is that value stocks have now drifted into the “higher beta” category. Betas above 1.0 indicate that a company’s stock price is more sensitive to moves in the overall market. Historically, growth stocks have been higher beta plays, but that has recently shifted.

- Quality, a characteristic typically marked by above average ROE, lower leverage, and relatively stable earnings, is another risk factor that has performed well. Companies of this nature align well with Appleton’s high quality stock selection focus. We feel that balance sheet strength is particularly important in today’s environment as companies manage through uncertain economic conditions.

- All eyes are on Q2 earnings, with consensus estimates showing a 44% decline in S&P 500 earnings per share, and a 22% fall for all of 2020. Given the drop in forward estimates combined with a sharp rise in price, valuation levels are undeniably elevated. While P/E ratios do not have high short-term predictive power, they suggest that the margin for error has narrowed. Bulls are hanging their hats on two trends. Although 2020 analyst estimates have dropped at a record pace, this trend slowed dramatically in June. A healthy recovery is also anticipated in 2021, with analysts forecasting 28% growth. Accordingly, we will be closely monitoring forward guidance. With over a third of the S&P 500 suspending guidance, analysts have been left flying somewhat blind and a return of corporate guidance could introduce surprises. While we welcome greater clarity, remember the saying, “be careful what you wish for.”

- Economic reopening stalled in late June as several states reported spikes in COVID-19 cases and hospitalizations. In our view, the market so far has overcome these developments for several reasons:

- Deaths have fortunately not risen at nearly the same pace. The average age of new cases has fallen, while the medical community is now better prepared to help patients.

- Promising trial results offer hope that a vaccine may be available sooner than originally thought.

- There is very little appetite for another shutdown and investors appear to anticipate a much more targeted prevention approach (wearing masks, protecting the vulnerable) should additional steps be needed.

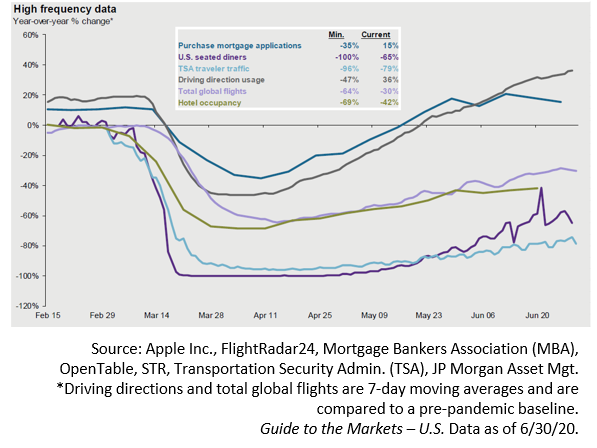

- As we evaluate recovery trends certain high-frequency data points will be revealing, including credit card spending, restaurant reservations, and road traffic. These data points had bounced back nicely, but more recent signs of weakness warrant close scrutiny.

- Investors are weighing major uncertainties, including the path of the virus, economic reopening, prospects for further stimulus, and geopolitical tensions. The upcoming election must also be added to the mix. Former Vice President Joe Biden is gaining momentum and betting odds show him in the lead, while the odds of a Democratic sweep in November are also increasing. The situation remains fluid, but investors will be reading the political tea leaves and processing potential policy impact as summer turns towards fall.

From the Trading Desk

Municipal Markets

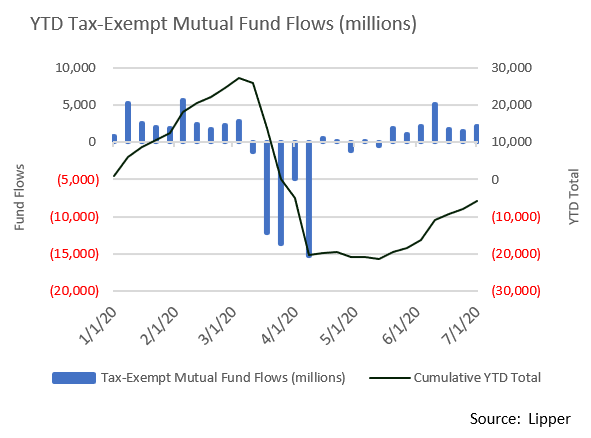

- Demand for municipals has been very strong with the past 7 weeks adding $15 billion of net fund flows, reducing YTD total net outflows to -$6.2 billion from a peak of -$22.1 billion earlier in the year. Long-term funds garnered more than half of these recent inflows. Intermediate and High Yield funds brought in $2 billion each.

- Over the month of June, yields moved slightly higher with the 10Yr AAA increasing 6bps, the 5Yr 3bps, and the 2Yr 11bps. While over the quarter, curve steepness from 2 to 10 years increased from 27 to 63 bps, and in our view, intermediate maturities continue to be more attractive than the short or longer term issues.

- Municipals still present relative value with the 10 Year AAA Muni/UST ratio ending the month at 134.3% after retracing earlier severe dislocation. The post-1990 average for this metric is 86.8%. Although nominal yields across fixed income asset classes are extremely low, the tax and yield advantage of high quality municipals relative to Treasuries is noteworthy.

- June issuance was up 23% over the same month last year as many issuers came to market that had been on the sidelines during the pandemic-induced volatility. Total YTD municipal issuance is now up 14.3% relative to 2019, much of which reflects taxable offerings where issuance is up 230% compared to 2019’s pace. Tax-exempt technicals remain supportive, with new money issuance falling 9.1% over the first half of the year.

Corporate Bond Markets

- Investment grade issuance continues to be incredibly robust as market tone and low rates are making funding attractive. The $169 billion of new bonds issued in June was more than double the $74 billion recorded during the same month last year. This year’s total issuance of $1.18 trillion is on track to easily surpass the record of $1.3 trillion set in 2017.

- Economic uncertainty and a desire to fortify balance sheets are not the only factors bringing issuers to market. Due to ultra-low UST yields and significant spread tightening, real IG Corporate yields are now lower than pre-pandemic levels. Strong, sustained demand and highly accommodative monetary policy are keeping funding costs extremely low, although COVID-19’s impact on the economy could slow activity over the 2H of 2020.

- Option-adjusted spreads have recovered nearly 200 bps of March’s dramatic widening. For example, the cost to issue a typical single A rated 5Yr corporate bond on 12/31/19 was 2.15%, 45bps more than 5Yr UST bonds at that time. As of 6/30/20, the same IG Corporate bond was yielding 0.95%, 66 bps over a compressed 5Yr UST yield of 0.29%.

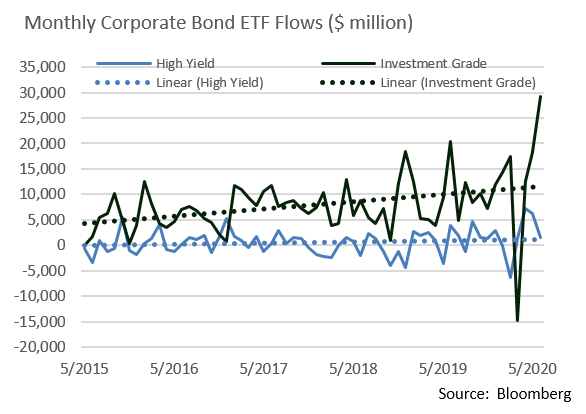

- Retail flows over the last several months have been very strong, thereby bolstering market values. After incurring nearly $15 billion of outflows earlier this year, ETFs regained most of that ground in April by gathering $12.5 billion of net inflows. May took in $18.25 billion and June an astounding $29.25 billion. YTD net flows into IG bond ETFs of $76.96 billion greatly exceeds $56.45 billion realized over the same period last year.

Financial Planning Perspectives

The CARES Act and Required Minimum Distributions: Understanding IRS Guidance

On June 19, 2020, the IRS issued Notice 2020-50: Guidance for Coronavirus-Related Distributions and Loans from Retirement Plans under the CARES Act. This guidance extends the availability of financial relief relating to Coronavirus-related Distributions (CRDs).

Qualification for Relief

The CARES Act allowed individuals to draw upon their retirement accounts to help alleviate economic distress, a subject we discussed in April’s Review & Outlook. Notice 2020-50 details a much wider range of hardship factors in identifying “qualified individuals” eligible for CRD relief.

A “qualified individual” is a person who “is diagnosed, or whose spouse or dependent is diagnosed, with the virus SARS-CoV-2 or the Coronavirus disease 2019 (collectively, “COVID-19”) by a test approved by the Centers for Disease Control and Prevention” and experiences adverse financial consequences as a result of their or a member of their household’s illness. These adverse financial consequences now include:

- Being quarantined, furloughed or laid off, or having work hours reduced due to COVID-19;

- An inability to work due to lack of childcare due to COVID-19;

- Closing or reducing hours of a business that the individual owns or operates due to COVID-19;

- Having pay or self-employment income reduced due to COVID-19; or

- Having a job offer rescinded or start date for a job delayed due to COVID-19.

The Notice allows employers to decide whether to implement the guidance relating to the CRD rules (which also includes safe harbor loan provisions for employers and provides guidance that allows employers to rely on an individual’s self-certification as a “qualified individual”). The IRS confirmed that “qualified individuals” can claim the full benefits of the CRD rules even if their employer does not change or update their retirement plans.

Required Minimum Distributions

The IRS followed on June 23 by releasing Notice 2020-51: Guidance on Waiver of 2020 Required Minimum Distributions. The Notice offers several potential benefits:

- The 2020 deadline that taxpayers who are RMD eligible face to roll over previously withdrawn funds from their retirement plans was extended to August 31 (previously July 15);

- Adds an ability to roll over funds taken in January;

- Waives the “once per year rule for rollovers” for RMDs repaid in 2020. This now allows eligible individuals receiving monthly RMD payments to roll over all their 2020 monthly RMDs taken to date as opposed to only one such distribution;

- Non-spousal beneficiaries can also now roll over 2020 RMDs from inherited IRAs.

For more information, we recommend:

https://www.irs.gov/pub/irs-drop/n-20-50.pdf

https://www.irs.gov/pub/irs-drop/n-20-51.pdf

Appleton’s Financial Planning Webinar Series Will Continue in September:

“Massachusetts Estate Taxes: Proactive Planning Matters” (Sept. 15, 2020)

“Financial Consequences of Adulthood” (Sept. 22, 2020)

Registration is open on our web site.

Email promotion that includes registration links will also be circulated later this summer.

For questions concerning our financial planning or wealth management services, please contact

Jim O’Neil, Managing Director, 617-338-0700 x775, [email protected]