Insights and Observations

Economic, Public Policy, and Fed Developments

- The most impactful development in a busy month of macro news came at the end when, after a strong CPI report roiled the markets, Fed Chairman Powell indicated in Congressional testimony that he no longer expected inflation to be transitory. Powell stated “…we’ve seen the factors that are causing higher inflation to be more persistent,” and that it would likely be appropriate to speed the pace of asset purchasing tapering. We agree, as “transitory” inflation was predicated on an end to the pandemic that has not yet occurred. However, we believe Powell’s remarks are likely being misread by a market that quickly began pricing in faster Fed Funds rate increases.

- First, Powell has pointedly refused to link the end of tapering with the start of interest rate increases. Second, while noting inflation had spread, he was careful to emphasize that “pandemic-related factors”, not an overheated economy, are behind more persistent price pressures and that raising rates will not defeat COVID-19. Both the Fed and market forecasters also agree that absent external shocks inflation should slow in coming months. The market may be basing rate expectations on today’s inflation levels rather than post-taper. While some FOMC members are open to 2022 rate hikes, we feel rate increases are not yet likely.

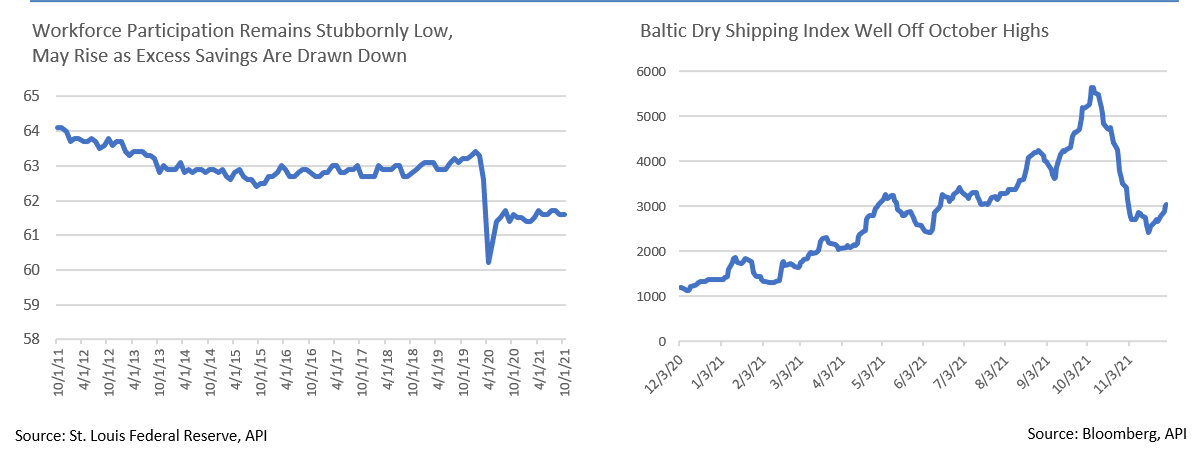

- Market-based metrics continue to support the argument that we are likely past “peak inflation,” and pandemic supply chain issues are easing. The Baltic Dry shipping index has fallen by nearly half since early October and appears to be stabilizing, easing one source of price pressure. Industrial production now exceeds pre-pandemic levels and, due to capacity utilization that still falls 3.2% below normal levels, there will be further production gains as bottlenecks ease. Retail sales remain strong in nominal terms but are close to flat in real terms. This is despite a holiday season pushed forward to allow for shipping delays, suggesting demand may not be able to drive inflation much further. And finally, in an unprecedented move, the Biden Administration approved the release of oil from the US Strategic Reserves in concert with China, Japan, India, South Korea and the U.K., a policy response that should ease energy prices.

- A new wrinkle for the global recovery lies in the Omicron variant, whose discovery roiled global markets on Black Friday. It is too early to say how severe this variant will be and what sort of impact it will have on public health and the markets, but the development is concerning and bears monitoring.

- An unemployment claims report of 194k on November 20th was the lowest since 1969 and spooked markets already wary of tight labor conditions. The reality may be more complex; Moody’s and Bloomberg separately estimated pandemic-era excess savings of roughly $2.6 billion, assets primarily held by the least wealthy 80% of US households. Bloomberg concluded that these excess savings may allow many US workers to remain out of the workforce through year-end, but after that time more will be pulled back into the workforce. If so, labor participation should begin improving in coming months. Already, there are encouraging signs in the household survey, where the number of Americans reporting they were unable to work due to the pandemic fell substantially in October, from 5.0 to 3.8 million.

- We welcome Chairman Powell’s re-nomination and believe he will easily be reconfirmed. Beyond his excellent track record over the last four years, it was also a symbolic and intentional move to shore up the Fed’s independence by returning to the tradition of the President appointing a Fed Chairman of the opposing party that had long been the norm before the Trump Administration.

Equity News and Notes

A Look at the Markets

- The S&P 500 built on the prior month’s gains for most of November, hitting an all-time intraday high prior to Thanksgiving on news that Jay Powell would be nominated as Fed Chairman. Those gains were quickly erased over the final three trading days, reducing YTD total return to a still impressive +23.2%. The reversal was sparked by news of an emerging COVID variant, followed by Powell surprising markets with talk of speeding up a scaling back of Fed asset purchasing.

- On the Friday following Thanksgiving, Omicron was officially listed as a “variant of concern” by the WHO and investors were quick to sell well before clarity regarding economic impact could reasonably be projected. Investors were already on edge given news of renewed lockdowns in Europe. Economic and mobility restrictions, particularly in Asia, could strain an already compromised supply chain, so the risk is real. Nonetheless, we do not believe US lockdowns of significance are likely given today’s much greater vaccination levels, far superior medical knowledge and tools relative to early COVID days, and minimal political will. Near-term volatility is likely to remain elevated though in the absence of specifics concerning Omicron’s transmissibility and virulence.

- Arguably, the more bearish news came with Powell’s comments on Capital Hill on the last day of the month. As discussed on the preceding page, Chairman Powell acknowledged that the risk of higher inflation had risen and stated that the committee would likely discuss an earlier tapering process. Longer term, the question for investors is whether the Fed intends on pursuing rate “liftoff” immediately following the end of the taper, or does being hawkish on the taper give them cover to remain dovish on rates? We are in the latter camp and do not anticipate 2022 rate increases.

- In the short term, the Fed’s hawkish surprise pushed shorter rates higher while COVID concerns were dampening the long end of the curve. Cyclical stocks, particularly Financials, got hit hard as they are impacted by narrowing maturity yield spreads. With cyclicals under pressure, investors moved money into large-cap tech names recently viewed as safe-havens. With large market leaders benefiting at the expense of smaller companies, breadth has weakened, a trend associated with increased volatility.

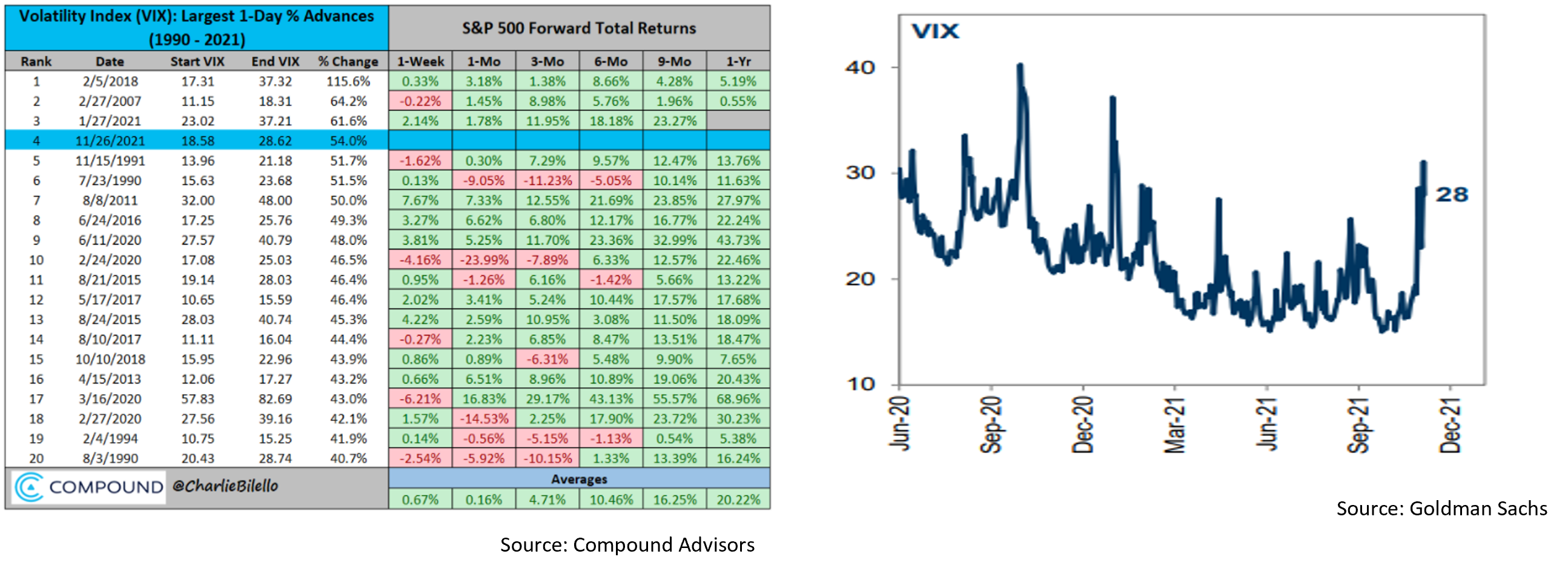

- Recent turbulence has come amid an atypically calm year. The historical average intra-year drawdown is -16%, whereas the maximum drawdown so far in 2021 was only -5.2%. The -2.3% decline on 11/26 may have been unsettling, but it was just the fifth > -2% day of the year as compared to a long-term average of about 9, and 25 in 2021. Wall Street’s “fear gauge”, the VIX, posted its fourth largest 1-day advance in the past 30 years. While elevated VIX readings often occur during down markets, forward returns from similar past moves have been strong, as demonstrated in the accompanying chart. It bears repeating that volatility is a feature, not a bug, of the market.

- The market feels vulnerable to headlines with uncertainty around COVID-19, Fed policy, and inflation as we head towards year-end. Should Omicron prove to be less severe than feared and follow the path of prior variants, we could see typical seasonal stock market tailwinds form. Questions concerning inflation and Fed policy will take longer to solve. We have seen signs of supply chains easing as commodity and shipping costs have come off their highs. While asset purchase tapering is considered tightening at the margin, the Fed will still have close to $9 trillion on its balance sheet by the time they stop buying and should remain historically accommodative.

- Fundamentally, the economy continues to recover, led by a resilient consumer, corporate profits are grinding higher (although we will be watching margins), negative real interest rates are pushing investors into risk assets, and both the consumer and corporations remain flush with cash that supports corporate buybacks and a “buy-the-dip” mentality. All of these factors are likely to fuel a healthy demand for stocks.

From the Trading Desk

Municipal Markets

- Demand continues to bolster the municipal market as we move towards the end of the year. The short end of the curve has been anchored for over a month, although intermediate maturities have recently demonstrated strength and incremental performance. The spread between AAA 2 and 10-year maturities narrowed in November to 79 bps but remains steeper than at the start of the year.

- Mutual fund flows have been consistently positive throughout the year, although there are signs that relentless demand is slowing. The highest weekly inflow in November was $2.6 billion, while the last week of the month totaled only $160 million. For the full year, inflows of almost $97 billion have helped keep yields at compressed levels. Looking into 2022, we expect retail demand to remain robust, a dynamic influenced by a sustained desire for tax-advantaged income and strong credit conditions.

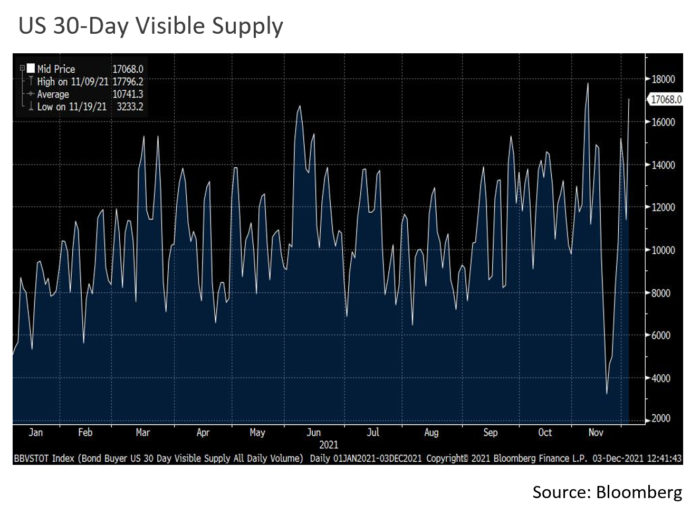

- The Thanksgiving lull helped produce a thin new issue market. Looking forward, 30-day visible supply of $17 billion is well above the YTD average of just under $11 billion and reflects issuers looking to get deals done before year-end. We welcome new supply as greater deal flow can be helpful in positioning portfolios ahead of the new year.

Corporate Bond Markets

- After yields fell at the start of November on Powell’s dovish press conference and a surprise decision not to hike by the Bank of England, the Treasury curve began to behave as if it wanted a reason to rise yet was not particularly concerned what that rationale might be. Yields first began to drift up after a surprisingly hot CPI report and continued after Powell was renominated, the latter based largely on concerns he would be less accommodative than Lael Brainard might have been.

- The tide quickly changed as Black Friday news of the newly discovered Omicron variant crushed Treasury bears. The 10Yr fell 13bps from its mid-month high, and the spread between 2s and 10s flattened 12bps. While it seems the default price action here would be a move to higher rates, we believe this flight to quality will hold at least until more is known about the latest variant, and the near-term probability leans towards lower, not higher, rates.

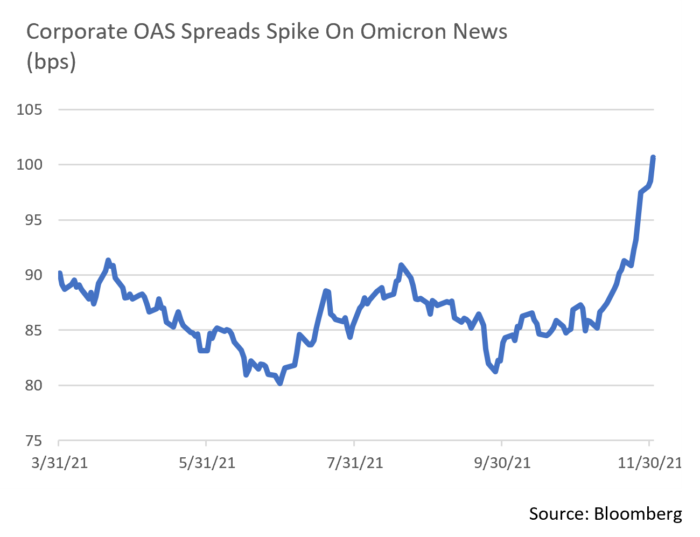

- The Omicron variant also broke spreads out of a tight ~10bps trading range. While a pre-Thanksgiving rush of issuance had softened the market and led to a modest backup in spreads, this was mostly evident in new issue concessions widening a little and deals modestly less oversubscribed than recent norms. On Black Friday, virus fears hit a thin half-day session and pushed spreads to their widest levels since early spring. The selloff continued into the start of December, with the Bloomberg Barclays US Corporate Index OAS rising to its highest level since this time last year. Despite currently high volatility, spreads remain reasonably tight and have remained remarkably resilient throughout 2021.

- With issuers able to borrow at historically low costs, 2021 is already the second largest year on record for IG corporate issuance, behind only 2020’s pandemic fueled borrowing spree. With a good number of companies deferring late November issuance until the markets settle, the all-time December record of $57 billion set in 2014 could be in play. Coming off a strong year, 2022 IG issuance forecasts have generally called for a slight pullback, but it is worth remembering that 2021 was not supposed to be a heavy year of issuance either following 2020. Current trends may still have room to run, and we are not concerned about the market’s ability to digest new supply.

Financial Planning Perspectives

The DC Legislative Agenda: Ramifications for 2022 and Beyond

Build Back Better Act: State of the Debate

With the House narrowly passing the latest version of the Build Back Better Act (BBBA) and sending it to the Senate on November 19th, there is growing anticipation that the legislative proposal could make it across the finish line before year-end. However, several points of resistance may still derail President Biden’s sizeable social spending, climate, and tax package. A few pressing concerns include Senator Sanders’ (I-VT) opposition to the magnitude of the proposed SALT cap increase for high earners, a desire to significantly expand Medicare to include dental and vision benefits, as well as Senator Manchin’s (D-WV) resistance to the inclusion of paid family leave and various climate provisions. As referenced in last month’s Financial Planning Perspectives, please look for forthcoming updates on the BBBA and related Congressional negotiations.

2022 Tax Planning

On November 10th, the IRS released Revenue Procedure 2021-45 which provided 2022 inflation-adjusted figures for over 60 tax provisions (https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-2022). Several prominent elements include:

- The standard deduction for married couples filing jointly increased to $25,900, up $800 from 2021. For single taxpayers and married individuals filing separately, the standard deduction rose to $12,950, up $400. Heads of households will see their standard deduction increased by $600 to $19,400.

- The highest marginal income tax rate remains 37% for single taxpayers with incomes greater than $539,900 and $647,850 for those married filing jointly. The other 2022 tax brackets are as follows:

- 35% for incomes over $215,950 and $431,900 for married filing jointly;

- 32% for incomes over $170,050 and $340,100 for married filing jointly;

- 24% for incomes over $89,075 and $178,150 for married filing jointly;

- 22% for incomes over $41,775 and $83,550 for married filing jointly;

- 12% for incomes over $10,275 and $20,550 for married filing jointly; and

- 10% for incomes of $10,275 or less and $20,550 for married filing jointly

The Federal Gift and Estate Tax Exclusion was increased to $12,060,000 and the annual gift exclusion, the amount that can be gifted without filing a gift tax return, has expanded by $1,000 to $16,000.

Other good news includes a $1,000 increase in the amount that may be contributed to 401(k), 403(b), TSPs and most 457 plans to $20,500. Those age 50 and older are also entitled to an additional $6,500 “catch-up” provision.

Phase-out amounts related to the deductibility of IRA contributions have increased as follows:

- Single covered by a workplace plan increased from 2021’s range of $66,000 – $76,000 to $68,000 – $78,000;

- Married filing jointly covered by a workplace plan increased from 2021’s range of $107,000 – $127,000 to $109,000 – $129,000;

- As it relates to Roth IRA contributions, the phase-out range for 2022 increased from $129,000 to $144,000 for single taxpayers, and $204,000 to $214,000 for those married filing jointly.

For additional details, please see: https://www.irs.gov/newsroom/irs-announces-401k-limit-increases-to-20500

Required Minimum Distributions

Finally, for those clients who will be taking required minimum distributions (RMDs) from retirement accounts in the new year, the IRS will be utilizing new Life Expectancy Tables. These revisions will reduce RMDs, thereby giving individuals an ability to leave more of their retirement savings in tax-sheltered accounts. Tax planning is an important element of the planning process, and we invite any questions you may have.

For questions concerning our financial planning or wealth management services, please contact

Jim O’Neil, Managing Director, 617-338-0700 x775, [email protected]