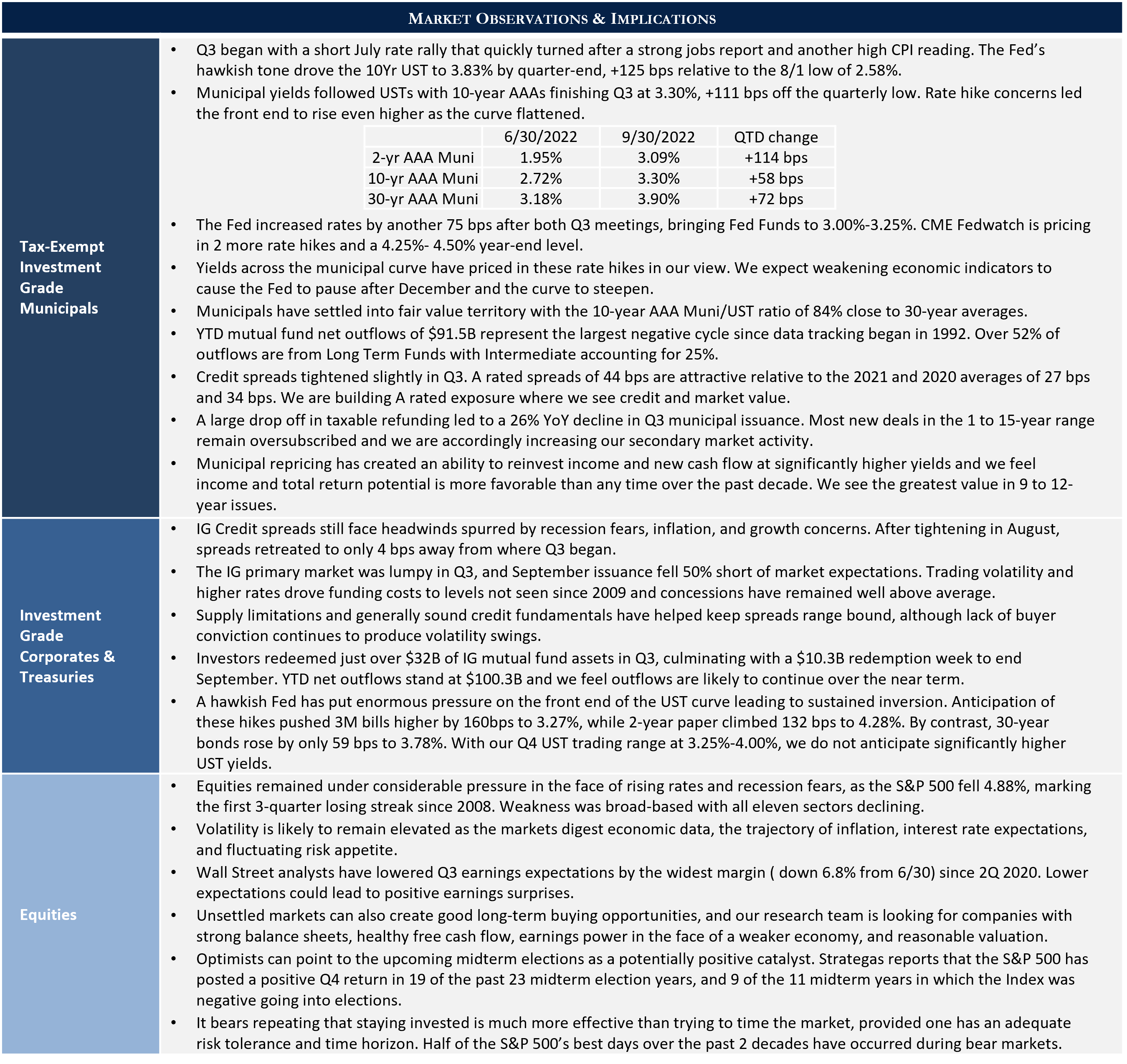

“Be fearful when others are greedy,

“Be fearful when others are greedy,

and greedy when others are fearful”

-Warren Buffett

Warren Buffett’s contrarian investment philosophy likely resonates with many who embrace a value-oriented mindset. While there is inherent logic in this time-tested recommendation, adhering to advice of this nature presents practical challenges. Sticking with an asset allocation strategy and rebalancing into risk assets during downturns is often the right approach, although doing so can be easier said than done.

The past three years have offered yet another stress test in our ability to deal with volatility. Those who sold under duress in early 2020, or later chased highly speculative momentum plays, risked compromising long-term returns. Volatility has clearly returned in the face of high inflation, rapidly tightening monetary policy, Russia’s invasion of Ukraine, and a very shaky global economic outlook. In this environment, helping clients avoid overly emotional reactions to turbulence is not easy, although gaining emotional insight can reduce the likelihood of doing the wrong thing at the wrong time.

The Roots of Investor Psychology

At their core, markets are a function of fundamentals and psychology. Last year we wrote about communication, understanding risk tolerance, and generational and experiential distinctions that influence investors. Let’s now focus on the difference between emotional biases and cognitive biases, as this may be useful in recognizing potential influences on one’s investment mindset.

Emotional biases involve basing decisions on individual perceptions and feelings that may cloud judgment. A few common ones include:

- Herding – crowd following, or buying what is popular without fundamentally based reasons;

- Loss aversion – a strong reluctance to acknowledge a mistake by realizing a loss;

- Overconfidence – excessive belief in one’s expertise in a given area;

- Endowment bias – overvaluing what you are familiar with.

Recognizing the extent to which you may be susceptible to various emotional pitfalls does not eliminate their influence, although considering these factors in dialogue with your portfolio manager can lead to better long-term decisions.

Cognitive biases involve decision-making based on preconceived notions that may not be accurate, such as:

- Anchoring – focusing on a reference point such as what you paid for a stock rather than what it may actually be worth;

- Recency bias – excessive attention paid to the most recent information received regardless of its relevance;

- Confirmation bias – seeking out information that suggests one is correct in an opinion and overlooking contradictory information;

- Small sample fallacy – drawing conclusions from potentially insignificant data points.

Cognitive biases can shade the perspective of both portfolio managers and individuals making their own investment decisions. Here too, mitigating their potentially harmful impact demands first recognizing our underlying thought process.

Step Back to Gain Broader Perspective

Warren Buffett has long advised investors to think of common stock shares as pieces of businesses to own over the long term, not as objects to be traded. At Appleton, our equity research process evaluates stocks with this in mind and looks at factors such as sustainability of a business model as well as valuation rather than focusing on tactical trading. We seek to mitigate analyst biases in part by bringing stock recommendations to the Equity Investment Committee before names are approved.

Self-awareness is a valuable trait, and we admit to not having unique market timing expertise. Instead, our equity investment process relies on proprietary research to minimize the influence of emotion or overly short-term thinking. We look for opportunities to purchase or add to stocks our team likes on a fundamental basis when the market gives us an ability to do so at attractive prices. Capital markets history has long demonstrated that a company’s market price tends to fluctuate much more rapidly than its business prospects. In essence, short-term perceptions are usually more volatile than long-term business value, a dynamic that speaks to the need to stay grounded during challenging periods while also not abandoning risk constraints during speculative times.

Most importantly, each client’s asset allocation plan serves as a foundation around which investment strategy is developed and employed. Unless there is a compelling reason to adjust course, staying with a well-designed, risk-managed plan is a good way to reduce the risk of emotions and biases clouding investment judgement. In fact, it may come as a surprise that half of the S&P 500’s best days over the last 20 years have come during bear markets.

A Personalized Approach

When working with clients on investment strategy, our Portfolio Managers first attempt to set expectations. In our experience, goals-based planning makes investment strategy more tangible and less susceptible to emotion. Communication is also essential, which is why we emphasize collaborative, accessible client service.

Like any other aspect of psychology, individual responses to market stress differ considerably and some investors struggle with turbulent markets more than others. “Tuning out the noise” is a challenge for many, but one that we feel can be mitigated by better understanding your investment psychology, falling back on a disciplined, risk-based asset allocation plan, and working closely with your Portfolio Manager. We’re here to help in any environment, so please do not hesitate to reach out with questions or concerns.